4.4.1 Extended enterprise value cycle

We began with a simple box with a transformation written in it (in Figure 19). Now we can start to bring some components we have explored so far together into an extended value enterprise cycle.

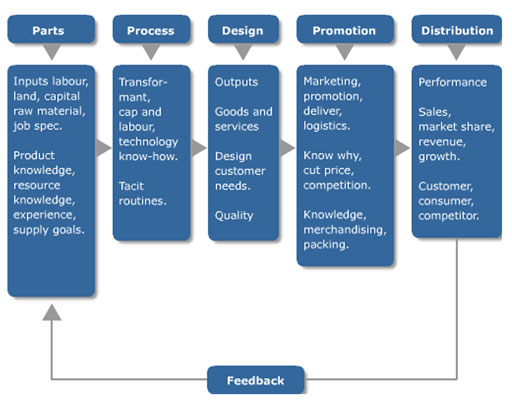

The parts or inputs that start the enterprise value cycle can be tangible, e.g. raw materials, buildings, etc., or intangible, e.g. knowledge or experience about something physical, like a product, or of a process.

The process uses specified or planned, and unspecified or tacit routines in changing the form of the inputs. Tacit routines can be particularly relevant and important in a small family business where each family member has their own job, that they do without thinking about it and certainly not writing it down.

The design element of the process is concerned with the goods and services that form the outputs of the transformation. They reflect the needs of the customer, the quality required and so on.

Promotion includes the presentation of the output. This could be the packaging of a product or the presentation of a service. It includes an awareness of competitor activity, including price and distribution channels.

The physical distribution is the last piece in the chain and results in the sale of the product or service. That is not all, though; it also includes an awareness of market position, growth trends and an understanding of both customers and consumers in their approach to purchase. This model builds on the inputs–outputs transformation model we looked at earlier in this section.

Value is added at each stage of this cycle but is only realised at the end. It is dependent on having the appropriate resources for your business and the capabilities that turn them into a product or service that can be delivered to the market in a sustainably competitive way.

The way in which you acquire your capabilities and skills – whether full-time, part-time, temporary or freelance staff or outsourcing to another firm – are determined by when and for how long you need particular capabilities and skills.

For example, if you were to decide that skills in financial planning and raising finance are needed for the launch period, but only for a few hours a week, it would be pointless to employ a full-time accountant. Equally, one with the range of skills required is unlikely to be in the market for a part-time job. In such a case, you would almost certainly be better off using an accountant in professional practice. It is also important to review the timing, quantity, level and frequency of need for each of the skills you have identified, and determine how each is to be introduced.

As you determine what you need, keep in mind the value that is added to your product or service at each stage of this process. This will serve to keep you focused on the costs associated with each step and also on the overall value of the knowledge you acquire, as well as the product or service you produce.