Week 1: Why and how should we invest for the future?

Use 'Print preview' to check the number of pages and printer settings.

Print functionality varies between browsers.

Printable page generated Monday, 29 June 2026, 12:01 PM

Week 1: Why and how should we invest for the future?

Introduction

Welcome to Week 1 of Managing my investments. Martin Upton of the Centre for the Public Understanding of Finance at the Open University Business School, presents a summary of the subjects and issues that will be explored during the next six weeks. Martin is a specialist in personal and corporate finance, and will guide you through this free course.

Transcript

In this first week you will explore:

- the current features and recent record of personal investment activity

- the first building blocks for constructing an investment strategy

- the factors that determine the levels of interest rates – one key determinant of investment returns

- the driving forces of movements in share prices – another key determinant of investment returns.

In examining these subjects, you look closely at recent trends in interest rates and share prices and the specific factors that have recently impacted on their levels.

At the end of the week you will have an understanding of personal investment behaviour and two of the most important determinants of returns you get from investing.

Throughout the course you will see some terms in bold. You can find definitions for these terms in the course glossary.

The production of this course was made possible by the financial help of True Potential LLP, who donated £1.4 million to enable The Open University to develop a free personal finance education programme for the public.

Before you start, The Open University would really appreciate a few minutes of your time to tell us about yourself and your expectations of the course. Your input will help to further improve the online learning experience. If you’d like to help, and if you haven't done so already, please fill in this optional survey.

1.1 Savings and investments

In Charles Dickens’s book David Copperfield, Mr Micawber infamously mused that an annual income of £20, coupled with an expenditure of £19, 19 shillings and sixpence (leaving sixpence over to save) was happiness itself. Whereas the result of spending £20 and sixpence (and having to borrow the difference) would be misery. Linking happiness or misery to having surplus income or surplus expenditure may be somewhat simplistic, but for many people having spare income, and thus an ability to invest for the future, can indeed help make life easier and more rewarding.

This course starts by looking at the importance of savings, why households save and invest, and the features of personal investment activity in the UK. We begin by defining some terms you are going to come across.

First, we want to draw a distinction between the definitions of saving and savings. Saving refers to a flow of money in a particular time period – such as putting money into a building society account. By contrast, savings (note the plural) are the current value of the total accumulated sum of previous saving. Savings are therefore the value of the stock of such savings that a household has at a particular point in time. Saving is connected to savings because saving in any given time period will add to the accumulated stock of savings. Consequently, if I already have £100 in a savings account, that £100 is my savings, but if I put an additional £25 a month into the account, I am saving £25 a month – after two months, my savings will have increased to £150 (plus any interest – the return paid on savings – earned).

We use the terms ‘saving’ and ‘savings’ in the same way as the UK Government’s official definitions, to encompass putting money into both ‘savings products’, such as deposit accounts, and ‘investment products’, such as shares, government bonds, and investment funds – including pension funds. However, you will notice that this section is called ‘Savings and investments’. This is because in personal finance a distinction is often made between the two with savings being associated with money held in bank and building society accounts, while investments relate to money held in shares, bonds and funds.

A key point about saving is that it defers (or puts off) consumption today in favour of consumption at some time in the future. This future may be a night out or holiday in the coming months or year, or even many years away in the case of a young person saving for retirement. Saving can even be for after death, such as when people save in order to bequeath or leave money for their children. This contrasts with the taking out of debt, which is bringing consumption forward by buying now and paying later.

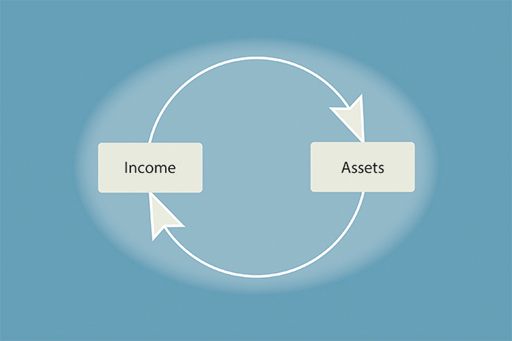

You should also note the relationship between assets held in the form of savings and investments and income. The receipt of income immediately adds to assets, for instance, when income is paid into a bank account. Such assets may only be temporary because the money is then used in the typical outgoings of a household, paying bills and living expenses, but any surplus income that isn’t used adds to a household’s savings and other assets. In turn, assets like savings usually produce an income in the form of interest on a savings account, for example. This interrelationship is summarised in the diagram above.

One other important point to note is that households often have debts and savings simultaneously – they are not mutually exclusive. For example, many households have a mortgage and a savings account. They can also be saving (for example, contributing to a pension fund) and taking on more debt (for instance, adding more to a credit card bill).

1.1.1 Why should we save and invest?

Saving and investing defers consumption from the present to a time in the future. Therefore, when thinking about the reasons for households to invest, we’re really thinking about why households are deferring consumption rather than consuming now.

One important reason for saving is known as the ‘precautionary motive’ – perhaps more commonly known as ‘saving for a rainy day’. This involves building up funds to provide for unexpected events and bills. If you have no savings and an unexpected event with financial consequences occurs (such as a car being damaged or someone becoming too ill to work and losing their income), then there are only three alternatives:

- receiving a payout from any insurance taken out against such an unexpected event

- borrowing money (from family, friends or financial institutions) to pay the unexpected bills

- defaulting on any commitments, for example not making payments on a car loan or a mortgage, with the consequent risk of repossession and negative impact on future credit ratings.

Having funds set aside in investments is an important means of preparing for unexpected life events – the savings act as a buffer to protect a household against these other possibilities.

A second reason for investing is to do so for a specific purpose. You can put a certain amount aside each month (or week), based on a calculation of how much you need for a particular goal. One of the most significant purposes for saving is for retirement, but investing can also be for many other reasons, for instance saving for a child’s university education, sending money abroad to family or paying the costs of a nursing home for a parent. You can also invest money temporarily – normally in savings accounts – for events that occur in the relatively near future, like a holiday or Christmas, or for buying a car.

A third reason for investing could be to accumulate wealth for which, as yet, there is no defined purpose. The savings may later be spent on a variety of things, for example a second home, a series of holidays after retirement or leaving an inheritance to children.

These three reasons all underline an important overall aim of having investments – to give a sense of independence and autonomy to do things. Having sufficient funds in your investments could enable you to leave a job, to take a break for a few months. It could also enable you to do or buy things that you want, or to take advantage of opportunities that arise (such as being able to pay for education or start a business).

1.1.2 Why are savings and investments important for the economy?

Watch the video below to hear Anthony Nutt, an investment fund manager, talk about the importance of personal investments to the economy and the impact of economic policy on savings behaviour.

Transcript

As well as being important for an individual or household, investments are important for the broader economy.

There is interdependence between the household sector and other sectors of the economy, such as the corporate sector. For example, in the act of saving, households are not buying the goods and services that firms sell. However, by saving, households are placing money in financial institutions and this provides a potential source of funds for firms to expand and to invest themselves.

Governments also have an interest in household savings. One reason for this is that governments often spend more than the receipts they have from taxation – this was certainly the case in the aftermath of the 2007/2008 financial crisis which saw the UK government’s budget deficit (the difference between its tax receipts and government spending) rise to what was then a record level. The COVID-19 pandemic also led to the UK government – and many other governments – increasing their borrowing sharply to cover the cost of the measures introduced to support households and businesses. To cover such a shortfall, governments have to borrow, including directly from the public. Governments have encouraged people to put money into government savings schemes (and, effectively, loan the government money), such as National Savings and Investments Certificates and Premium Bonds.

1.1.3 Savings and the life course

Households are motivated to save at different stages of the life course, such as those depicted in Figure 4: weddings, holidays and motoring.

Households are often targeted by the marketing departments of financial institutions according to their stage in the life course and the type of household. These are significant factors in the selling of different types of saving and investment products.

Activity 1.1 Your reasons for saving

Think about the following questions and note down your answers.

- What are your reasons for saving money?

- Are your reasons for saving the same as any of those given in the image above?

1.2 Savings behaviour in the UK

So how much savings do UK households have?

The Family Resources Survey (DWP, 2023) provides evidence to explore this question. Remember, by referring to savings we mean the stock of such savings that UK households have.

| Savings | All households (%) |

|---|---|

| No savings | 13 |

| Less than £1500 | 26 |

| £1500 but less than £3000 | 8 |

| £3000 but less than £8000 | 14 |

| £8000 but less than £10,000 | 3 |

| £10,000 but less than £16,000 | 7 |

| £16,000 but less than £20,000 | 3 |

| £20,000 but less than £25,000 | 3 |

| £25,000 but less than £30,000 | 3 |

| £30,000 or more | 20 |

As you might expect, households have different levels of savings, with 13 per cent having no savings at all, while 26 per cent have savings of £20,000 or more.

The Office for National Statistics (ONS) has said that significant caution needs to be exercised when drawing firm conclusions from data on savings such as those presented above.

Activity 1.2 Caution

Why do you think the ONS might suggest such caution?

Make some notes in the box below.

Discussion

The responses provided to surveys where people have to provide personal information – particularly information about their finances – need to be treated with care.

The reason for the caution is linked to how data on savings is collected. Much official government data is based on surveys where households are asked to complete a questionnaire. An estimated one in four households simply does not know the value of its investments, while others may deliberately understate the value of any assets they have. Disclosing financial data can be seen as sensitive, and so collecting such data accurately can be problematic.

1.2.1 UK household investments (excluding pensions)

The table below provides a breakdown of the types of savings, investments and accounts that households have in the UK. As you can see, virtually all households have a current account, and a significant proportion have at least one form of savings account. Lower proportions of households have stocks and shares, and nearly one-sixth of households have investments in premium bonds. In 2021/22, four per cent of households had no kind of bank account, let alone any investments. You shall be looking at some of these products in more detail in Week 2.

| Type of account | % of households |

|---|---|

| Current account | 95 |

| NS&I savings account | 3 |

| Basic bank account | 3 |

| ISA | 31 |

| Other Bank or Building Society account | 47 |

| Stocks and shares/member of a Share Club | 11 |

| Unit trusts | 1 |

| Premium Bonds | 16 |

| National Savings Bonds | 1 |

| Company Share Schemes/profit sharing | 1 |

| Credit unions | 1 |

| Other | 1 |

| Any account | 96 |

| No account | 4 |

These figures are interesting, but do not tell us very much about exactly why some households have savings and other financial assets and others do not.

The Family Resources Survey provides investments by some of the social and economic variables such as income, household composition, age and ethnicity of households, and these can help explain the differences in household investment behaviour.

Some findings from the 2020 and the 2023 Family Resources Surveys are as follows:

- As might be expected, low-income households tend to have a lower value of investments and higher-income households have a higher value of investments.

- Households where the named head, or spouse of a household head, is unemployed or disabled are much more likely to have no investments at all.

- Pensioner couples, single male pensioner households, and couples without children tend to have higher investments, while single adults with children households have the lowest levels of investments.

- Asian and Black ethnic groups are slightly more likely to have no investments than White households.

Some of the above points remind us that investing will not be easy for everyone. It is easier to build up investments as household income increases. For those on lower incomes, investments have to be built up through careful budgeting.

1.2.2 The UK’s savings ratio

When looking at savings behaviour a key measure is the household saving ratio. This measures the percentage of household disposable income that is available to be saved – i.e. gross income after tax and other deductions and less household spending.

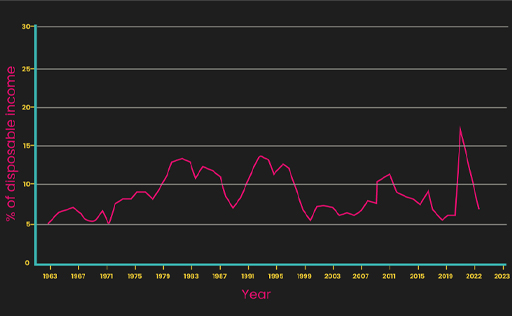

Figure 6 above shows the household saving ratio for the UK since 1963. It shows how the ratio has varied over this time. In 2020 the ratio was dramatically affected by the impact on the economy of the COVID-19 pandemic which reduced household spending and so increased the capacity of households to save money. The measure for 2020 also vividly demonstrates a key driver of the ratio – it tends to rise during periods of economic uncertainty or weakness. The increases in the ratio in the early 1980s and 1990s - and again after the financial crisis of 2008/9 - coincided with economic recessions in the UK. The evidence suggests that in such times households look to build up ‘precautionary’ balances of savings in case they are directly affected by these economic downturns.

By contrast when the UK economy was growing quickly (with household incomes rising), the household saving ratio was lower. This can be explained by the fact that when things are going well, confidence is high, and people tend to spend more. The diminished risk of unemployment when the economy is performing strongly reduces the perceived need for precautionary savings balances. This was the picture in the late 1980s and in the early 2000s.

1.2.3 How the housing market affects savings activity

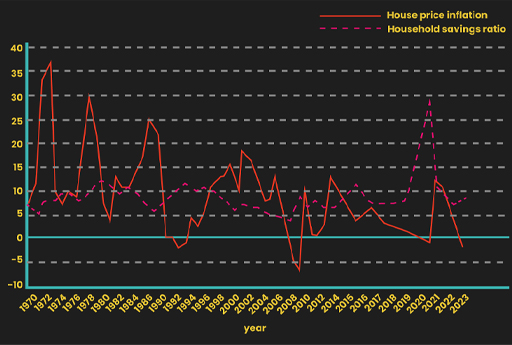

When examining investment behaviour, data suggests the state of the housing market may also be important. Figure 7 shows changes in the household savings ratio and changes in house prices in the UK between 1970 and 2023.

Activity 1.3 House prices and saving

Note your answers to the following questions:

- Look at the chart and consider any pattern between house prices and the household savings ratio.

- Can you think of any reasons to explain this pattern?

Discussion

There appears to be an inverse relationship between house prices and the household savings ratio. That is, when house price increases were higher (for example, in the late 1980s and most of the 2000s), the household savings ratio was lower, and when house prices were lower (for instance, in the early 1990s and 2009), the household savings ratio was higher.

This may be because people often feel that they do not have to save as much when their wealth is increasing due to the increased value of their house. Conversely, in 2009 there was an increase in saving as house prices fell and households repaid some of their borrowings. The fall in the savings ratio in the 2010s may be linked to the renewed rise in house prices. The data for 2020 was affected by the impact of the COVID-19 pandemic which boosted the savings ratio by reducing household spending.

1.2.4 Savings in an international context

The UK has a relatively low household savings ratio compared with other countries, as shown in Table 1.3.

| Switzerland | 21.9 |

| Ireland | 20.2 |

| Netherlands | 17.0 |

| Sweden | 15.5 |

| Germany | 15.1 |

| France | 12.8 |

| United States | 12.4 |

| European Union average | 10.1 |

| Japan | 7.8 |

| Italy | 7.6 |

| United Kingdom | 6.9 |

| New Zealand | 3.6 |

| South Africa | 1.1 |

| Portugal | -0.6 |

| Greece | -3.1 |

Footnotes

Notes: The ratio for the UK is measured differently to the measure used in previous sections of the course (largely due to the treatment of savings in pension schemes). Negative ratios indicate ‘dissaving’ (a reduction in savings).The data shows the household savings ratio varying significantly between countries. The data is cross-sectional – a snapshot of a moment in time. As a result, we cannot draw too many conclusions – for example, Portugal had a ratio of 2.1% in 2020 whilst in 2022 it had fallen to minus 4.9%.

Of particular interest, though, is that the UK’s ratio is lower than in those Western European countries that we would consider as economic peers: France, Germany, the Netherlands and Italy.

The reasons for these differentials are various. Cultural reasons are a key factor with some societies having a stronger tradition of saving and investing – sometimes due to the greater incidence of natural catastrophies. The financial strength of economies is also vital since households with growing affluence are better placed to have surplus income to save for the future. Access to finance is also critical: if you are confident of the ability to be able to borrow money to finance life’s major expenditures or to cover unexpected events, you may be less inclined to save to provide the funds needed to cover these.

1.2.5 Why aren’t we saving and investing more?

There are many factors that may explain weak savings behaviour.

- Falling real incomes – after the 2007/2008 financial crisis there was a period where the real value of earnings fell with wage rises on average being less than the prevailing rate of price inflation. This diminished the scope for surplus income to place in investments. Generally the growth of real incomes for UK households has been low in the decade since the financial crisis and, at the time of writing (in 2020), this is being exacerbated by the impact of the COVID-19 pandemic.

- Poor education – a lack of awareness of products and how to invest may also be impacting on personal investment volumes.

- Delayed benefits of investment – one key behavioural trait when it comes to money is a dislike of delayed rewards. Investing money for the future means forsaking consumption today – and this may deter people from making investments.

- Inertia – while most people know they need to invest for the future to provide for emergencies and a pension, many of us simply don’t get round to doing something about it until we are forced to do so.

- Low returns in recent years – low returns, specifically from savings accounts, may have encouraged many to spend money today rather than save for the future

- Access to debt if there is a need for cash – the continued and widespread availability of personal debt products, albeit some with exorbitant interest charges, may discourage savings. Why save when you can borrow money when needed to cover for a contingency or special occasion?

- The culture of impulse spending rather than impulse saving. Research has shown that adults in the UK spend, on average, £672 a year on impulse purchases. Investing this sum each year over the course of a working life could result in a material enhancement to the pension resources available on retirement.

1.2.6 Investment and retirement planning: the UK experience

To complete your review of savings and investment activity, watch this presentation by Alexandra Chesterfield, Head of Behavioural Insights at the consumer organisation ’Which?’. The video explores some features of, and shortcomings in, savings and investment behaviour (including pension planning).

Transcript

1.3 Investment planning needs a long-term perspective

You have now completed your review of savings and investment activity, with an emphasis on the UK. Clearly there is evidence of poor personal investment planning.

To avoid these pitfalls when it comes to our finances we now need to start thinking about how we should go about the business of effective investment management. Let’s build the foundations of an investment strategy.

Looking ahead – investment planning is a long-term activity

Investment planning means looking ahead – often a great many years ahead. Whether it is for a future major purchase or for retirement, the process of building up investments may take several years or even decades. This long-term time horizon requires us to assess a number of things.

First, it requires a forecast to be made of how inflation will affect the future cost of the item to be acquired or the level of income needed for retirement. When planning investments, it is crucial that inflation is taken into account (planning is done in ‘real terms’). This means that forecasts of future values should all be in terms of today’s money, so that you’re looking at what the money invested might buy after taking into account the possibility of price rises between now and cashing in the investment.

Second, the time horizon is vital in determining the structure of investments. If the horizon is the near future, there is little sense in investing in products that may fall in nominal value. The longer the time horizon, the greater the capacity to ride out periods when investments don’t perform well, in order to benefit from their gains over the medium to longer term.

Recalibration is also vital. Checking regularly (at the very least annually) that your investments are on track to achieve your goals is vital. If they are going off track then decisions may need to be made, including increasing the amount of current income diverted into investments (increasing the sacrifice of today’s spending to benefit from greater income in the future). Alternatively, the structure of the investment portfolio may need to be revised to improve expected performance over the chosen time horizon.

Even if you invest passively and let others (i.e. fund managers) look after the management of your assets, the responsibility for monitoring and managing the investment portfolio ultimately lies with yourself.

Filling the blank canvas

The planning process should involve:

- Starting with a blank canvas by not letting previous investment experiences and plans dictate what you plan to do now.

- Linking your investment plans to your life’s goals and the timing of these goals – for example, the time you expect your children to go to university and, consequently, require substantial financial support to ensure that they do not become over-indebted with student loans.

- Prioritising your goals. You cannot necessarily achieve all goals, particularly simultaneously, but you can have a list that comprises of ‘must haves’, ‘would like to haves’ and ‘would like to haves, if possible’.

- Taking into account that your investment planning is not a fixed plan that is set in stone. Rather, it is a living document that needs to be reviewed as circumstances change (which may increase or reduce both the need or the ability to invest for the future).

- Embedding investment activities into your life’s routines – for example, by setting up direct debits to make contributions to your investment funds monthly. This will avoid putting off, and perhaps ultimately not undertaking, investments that need to be made for the future. The default should be that you have to take action to stop investing, rather than having to take action to invest.

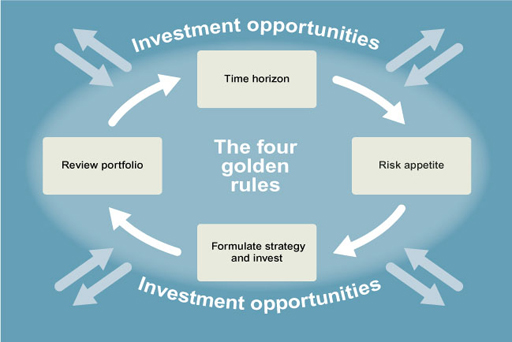

We can summarise this planning process through the four stage financial management model – a model that can be deployed for making all personal financial decisions including those relating to personal investments (Figure 10).

You can apply this financial planning model to your own decisions as you work through the course to help you build your investment strategy and compile your portfolio.

1.3.1 Retirement: the longest time horizon

Planning for retirement is the most important aspect of investment management.

The scale of the funds that need to be accumulated for a comfortable retirement dwarfs those needed for other investment goals like saving to buy a house or car, or to pay school fees.

The time span between commencing retirement planning and cashing in the investments to provide income in retirement can – and should – span decades rather than years.

Growing longevity also means that despite the choice of many to work well into their 60s, the time period spent in retirement is, on average, growing, with the related implications for the resources needed to provide an adequate pension income.

To consider how an individual or household can plan ahead for their retirement years, a robust financial planning model needs to be adopted and applied. This, or similar planning models, would be used by a financial adviser as the foundation for advice about retirement planning and provides an approach that you can also use for yourself.

Central to the situation is the goal of a comfortable retirement. The need is to have enough income throughout retirement to finance a certain standard of living. The amount required will be determined largely by expectations of spending in retirement.

This raises a question: whose spending needs? Should the financial plan look at the individual or the household? The danger of basing the plan on the household is that many households change over time as, for example, couples split up, family members and friends decide to share a home or leave, or people die.

Traditionally, married couples have adopted the household approach, and the resulting financial plans have often proved inadequate in the face of death or divorce. This is a key reason why women account for such a high proportion of the poorest pensioners today.

The advantage of a retirement plan based on the individual is that each member of the household has their own pension arrangements, which they retain even if the make-up of their household changes.

Spending in retirement can be estimated from the individual’s or household’s current level and pattern of spending. Yet there are some good reasons to think that spending in retirement may be different from spending while working, and that spending needs in early retirement may differ from those later on.

An alternative might be to base estimated spending needs on the spending patterns of current pensioners, but bear in mind that what today’s pensioners actually spend may reflect the constraints of the income they ended up with rather than the income they wanted to have.

Note that Week 5 of this course is entirely devoted to the key personal investment matter of pension planning.

1.3.2 Investment returns

The returns that are received from investing fall into two categories – income and capital growth. Income can come in the form of interest on savings accounts and bonds, or dividends on shares.

Capital growth can come in the form of the increase in the value of the assets – higher share prices, increases in indices for investments contractually linked to a market index (like a stock exchange index) and higher bond prices for those bonds that are marketable. For savings accounts, though, there is normally no potential for a growth, or risk of a decline, in capital value. The money placed into an account does not change in nominal value and the only returns received are the interest paid on the account.

Three particular factors need to be borne in mind when measuring and forecasting investment returns:

- All returns should be measured in real terms, not nominal, by accounting for the impact of price inflation on the value returned to the investor through income or capital growth.

- Assets whose prices can move can clearly move down in price in nominal terms as well as increasing in price. Care needs to be taken when investing in those assets with price sensitivity – particularly if the investment period is short. As you examine different types of investments in Weeks 2 and 3, you’ll see that there is a relationship between risk and return – this being that those assets that offer the greater returns, are associated with greater risks in terms of the volatility of the value of the investments and the prospect of default by the entity with whom the investment is placed. In Week 3 you’ll look closely at the types of financial risks investments may be exposed to and at how effective risk management is central to investment management.

- There is an inverse relationship between interest rates and the capital value of assets. A period of high interest rates may have the impact of depressing share prices due to the impact of high rates on economic activity and hence on the performance of companies and, by consequence, their share prices. For some assets, like fixed-rate bonds, there is a certain mathematical relationship between interest rates and asset prices: if interest rates rise, bond prices will fall (and vice versa). You’ll learn more about this in Week 2.

Investment returns – tax breaks and tax wrappers

A crucial element to factor into investment planning is the tax treatment of the returns. Some investments have what is referred to as a ‘tax wrapper’, where the returns are protected from tax of either the income they generate or any gains to capital gains. The most common example of these in the UK are Individual Savings Accounts (ISAs) where returns are tax free (with the exception of the taxation of dividends received on Stocks & Shares ISAs). Elsewhere, even where investment returns are subject to taxation, annual tax-free allowances can be used to protect at least part of the returns from tax deductions. You’ll look at the tax treatment of returns from personal investments in the UK in more detail in Week 2. At this stage, the key point to note is that for your preferred form of investment you should make sure that you take advantage of any tax exemptions on their return.

1.3.3 Drivers of returns: what determines the level of interest rates?

Earlier you started to look at the income and capital returns from investing. You will look more closely at these now, starting with the key issue of what determines the level of interest rates on savings and investment products.

To understand what determines the level of interest rates received when you invest money, you first need to understand how ‘official’ interest rates are set.

The video, which features Mark Carney, Governor of the Bank of England at the time of writing this course, sets the scene by looking at the factors taken into consideration when setting official interest rates.

Transcript

Before 1997, ‘official’ interest rates in the UK were determined by the UK government, usually after consultation with the Bank of England. Arrangements changed in May 1997 when the incoming Labour government passed responsibility for monetary policy and the setting of interest rates to the Bank of England to make the bank independent of political influence. This matches the arrangement in the USA and in the eurozone, where the official rates are set by the Federal Reserve Bank and the European Central Bank respectively.

The rate set by the Monetary Policy Committee (MPC) known as the ‘Bank Rate’ is the rate at which the Bank of England will lend to the financial institutions. This, in turn, determines the level of bank ‘base rates’ – the minimum level at which the banks will normally lend money. Consequently, Bank Rate (also known as the ‘official rate’) effectively sets the general level of interest rates for the economy as a whole. Bank Rate is therefore hugely influential in the determination of the rate that will be paid on savings and interest-bearing investment products.

The MPC meets eight times a year to determine the level of Bank Rate with the decision normally being announced at 12 noon on the day that their two-day meeting ends (which is normally a Thursday).

The prime objective is for the MPC to set interest rates at a level consistent with inflation of 2% p.a. For example, if the MPC believes inflation will go above 2% p.a., it might increase interest rates in order to discourage people from taking on debt – because if people spend less, it could reduce the upward pressure on prices. Conversely, if the MPC believes inflation will be much below 2% p.a. it might lower interest rates (also known as ‘easing monetary policy’) – people might then borrow and spend more.

However, in 2013 and 2014 the policy on the setting of official rates was modified to take greater account of the level of unemployment in the economy. First it was announced that official rates would not be raised while the rate of unemployment was above 7% of the labour force. Subsequently, following a sharp fall in unemployment towards 7%, this stance was modified to one where the MPC would take account of the extent of spare capacity in the economy rather than just the rate of unemployment. The video explores this change of emphasis to the setting of official interest rates in the UK.

Official rates of interest tend to be cyclical, rising to peaks and then falling to troughs. Since 1989, the trend in the UK has been for nominal interest rates to peak at successively lower levels. Bank Rate fell to 3.5% in 2003. In 2009 it was set at a then historic low of 0.5% as the Bank of England attempted to stimulate the economy during the period of economic recession that followed the 2007/08 financial crisis. Bank Rate stayed below 1% for the next decade only to fall to a new historic low of 0.1% in 2020 as the Bank responded to the economic problems caused by the COVID-19 pandemic.

From late 2021 Bank Rate was raised in stages to reach 5.25% in September 2023. This tightening of monetary policy stemmed from the need to combat the high prevailing rate of price inflation in the UK.

1.3.4 Real interest rates

You explored earlier why it is important to take inflation into account when managing your investments. Unless there is no price inflation, the nominal return from an investment – the amount of cash paid to you – is different to its real return, in effect the value to you in terms of the goods it can buy.

Real interest rates are interest rates that have been adjusted to take inflation into account. Looking at the graph, you’ll see that when inflation is higher than the nominal interest rate, real interest rates are negative (as they were in 1980/1981 and again from 2010). Real interest rates are at zero when the rate of inflation and the nominal interest rates are the same, and they are positive when the nominal interest rate exceeds inflation.

Real interest rates were low in the 1990s and 2000s, falling from 7% in 1990 to just under 2% by 2004. Subsequently they fell further. By early 2015 the fall in the (nominal) official interest rate to the then historical low of 0.5%, combined with price inflation of 1.4% (as measured by the Retail Prices Index – RPI), resulted in a negative real interest rate of -0.9%. Indeed, low nominal rates of interest meant that the UK experienced negative real interest rates throughout the 2010s and, particularly, in the early 2020s.

So, if you earn a nominal rate of interest of 1.5% on your savings and price inflation is 2%, you are actually getting a real interest rate on your savings of -0.5% – a negative rate of return. Such a situation where real interest rates are negative is clearly adverse for savers. However it is good news for borrowers if the cost of borrowing is negative in real terms.

Unsurprisingly, the low interest rates offered on savings in recent years have encouraged some households to reduce their debts – particularly credit card debts which have relatively high interest rates – by reducing their savings balances.

1.3.5 The benefit to savers of compound interest

The calculation of interest on savings accounts is straightforward. Interest accrues at a rate based on the savings rate and the balance of money in a savings account. So if £1000 is held in an account where the rate is 5% per annum then interest paid at the end of the year is £1000×5/100=£50.

In many cases, with movements into and out of savings accounts taking place, the interest charged will be based on the average balance of the principal sum during the year. For instance, if £10,000 is invested at the start of the year and £100 is withdrawn halfway through each month, then the outstanding balance at the end of the year would be £8800. The average balance of principal outstanding during the year would be the average (mean) of the balance at the start and at the end of the year, or (£10,000+£8800)/2=£9400. Based on this average balance, the interest for the year at 5% p.a. would be £9400×5/100=£470 – less than the £500 that would have been received if no withdrawals had been made.

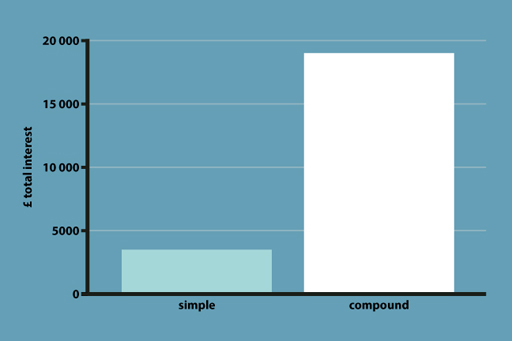

What happens if the lender does not withdraw the interest received and adds it to the balance of the account? This would mean that the following period’s interest earnings is going to be higher since the borrower will be paying interest, not only on the original principal sum but also on the re-invested interest. This is known as compounding, and can quickly enlarge savings during periods of high interest rates.

Consider what happens if someone lends £1000 at an interest rate of 3.5% and makes no withdrawals over ten years. Over this period of time, the investment would rise from £1000 to £1411 (£411 interest on top of the £1000 invested). This is more than if interest had been charged on a simple rather than compound basis – simple interest over ten years would have been just £350.

You can test this out for yourself, using our interest calculator .

The precise practice for computing the interest earnings varies among different borrowers – and interest can be calculated at different time intervals. One of the pieces of financial small print it is always vital to read is the basis on which interest is paid – that is, how often and by reference to what terms.

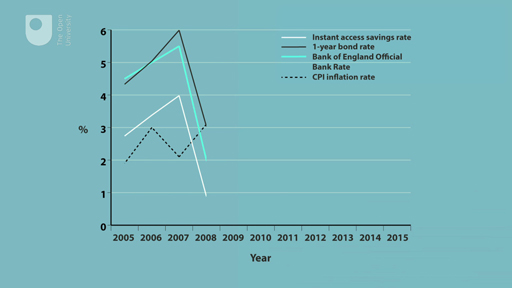

1.3.6 Case study: whatever happened to UK savings rates?

A major development that affected millions of investors in the UK after 2007 came with a fall in interest rates paid on savings accounts.

The audio and the supporting graphics in the video below set out the decline which resulted in investors earning less than the prevailing rate of price inflation with the consequence that the real value of their savings ended up being reduced. The causes of this development are explained in the audio.

The episode is both a classic case of macro-economic policy having both winners and losers and of the realities of inflation risk on investments. Faced with such meagre returns many investors turned to alternative investments to boost their income – but in so doing took on a variety of alternative investment risks.

While the audio covers events in the first half of the 2010s the issues it identifies remain relevant today. The general level of interest rates is determined by the Bank of England’s official rate (Bank Rate) and the returns that savers can expect are therefore inevitably influenced by those economic factors that determine Bank Rate – principally the levels of price inflation and economic activity in the UK.

Transcript

1.4 The drivers of equity markets

You have seen the factors that can dictate the prevailing level of interest rates in the economy and by inference the returns on interest-bearing investments.

So what drives the levels of share prices? While you will look at share price determination in detail in Week 2, it is important to get a grasp on the key determinants here at the start of the course.

The first important point is to distinguish between the factors that will generally affect the levels of share prices – typically measured by referring to stock market indices like the FTSE 100 (the index comprising the 100 largest companies listed on the London Stock Exchange) – and those factors that specifically affect a particular, individual, share price.

The key drivers of equity markets are:

- the prevailing and expected level of economic activity, as measured by GDP growth, employment levels and movements in the real incomes of households

- the prevailing and expected level of price inflation

- the prevailing and expected level of interest rates

- the trends in and expectations of the financial performance – particularly profitability – of the firms whose shares comprise the equity markets.

In addition to these core drivers, other factors that impact on equity markets include:

- movements in exchange rates

- changes to taxation – particularly on company profits and dividends paid to shareholders

- changes to commodity prices – particularly oil and gas

- random non-financial events like wars and disease epidemics, which are expected to impact on (global) economic activity.

These factors impact, to greater or lesser extents, on the financial performance and expected future performance of the companies whose shares comprise the equity indices that investments in shares are linked to.

A slowdown in economic activity, perhaps reflected in a weakening in price inflation, can be expected to reduce sales and profits. Under these circumstances, companies may be forced to reduce the dividends paid to shareholders or even pay no dividend at all. The attraction of holding shares, relative to other assets, is then reduced exposing the risk of a fall in share prices. The reverse generally holds as well – growing economic activity and a pickup (provided it is not excessive) in inflation are correlated to higher share prices as companies experience growing sales and profits. The relationship between inflation and the performance of stock markets is, though, complex and hotly debated by analysts.

Modest inflation may be favourable to share prices but higher inflation rates raise the prospect that action will be taken to stem inflationary pressures by raising interest rates and depressing economic activity – a scenario which would not be good for share prices. The other factors listed above also have a role in driving share markets. Higher interest rates are bad news for equities as they presage a decline in economic activity – as do higher commodity prices. If exchange rates move adversely – particularly if the domestic currency strengthens against foreign currencies – the equities can be hit since export sales may be reduced.

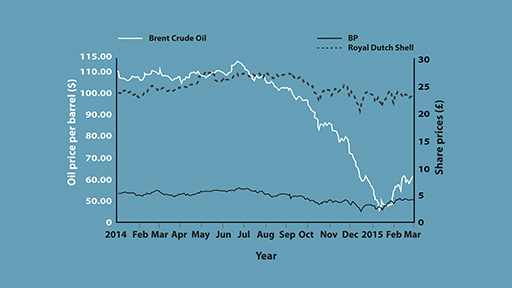

1.4.1 Oil prices and the financial markets

The collapse in oil prices in the second half of 2014 – with the price of crude oil halving between July 2014 and January 2015 – had a mixed impact on financial markets. Listen to the audio, a clip from BBC Radio 5’s ‘Wake Up To Money’ programme, to find out more.

Transcript

By helping to reduce the overall rate of price inflation, the fall in the price of oil virtually eliminated the risk of a near-term rise in interest rates. This was ‘good news’ for the financial markets – although not for savers. However, the fall in oil prices was seen by some commentators as indicating a slowdown in economic activity globally – a factor that is not good news for equity markets and certainly not good news for the share prices of oil companies.

1.4.2 Drivers of share prices: company specific performance

While the factors mentioned in the previous section provide the general drivers of share prices, the price of an individual share will also be driven by specific factors applying to the company in question.

Commonly, this means that the performance of an individual share outperforms or underperforms the average for the market as a whole. Sometimes this divergence can be so stark that the share price rises when the market as a whole is falling and vice versa. This differential performance is normally sourced in how the direction of company profits and dividend levels contrasts – favourably or unfavourably – with investors’ expectations and with averages for the market.

A classic recent episode in September 2014 came with the performance of the share price of the supermarket, Tesco. This plummeted after it was revealed that the company had been overstating its profits guidance to the markets, prompting a myriad of investigations, including one by the financial services regulator the Financial Conduct Authority (due to Tesco’s banking activities).

Within days Tesco’s share price was down by 30% from its 250p level at the start of the month, despite the fact that in September 2014 the overall level of the FTSE 100 was quite steady, falling by only 3%. Even the renowned investor Warren Buffet took a huge hit, given his 3.7% stake in Tesco, and within weeks he was offloading a proportion of his failed investment. Given the belief that Tesco will be forced to react by aggressive competition in the marketplace, the shares of other UK supermarket groups, like Sainsbury’s, also fell in the wake of the decline in Tesco’s share price – albeit not to the same degree.

Subsequent months saw Tesco announce a record annual loss for the financial year ending in February 2015 of £6.4 billion and a major overhaul of its senior management. Tesco’s share price fell to a low of just under 156p in early 2015, although by 1 May 2015 it had recovered to 225p.

Tesco was a classic case of the crystallisation of specific risk relating to the investment in a specific company as opposed to the market as a whole.

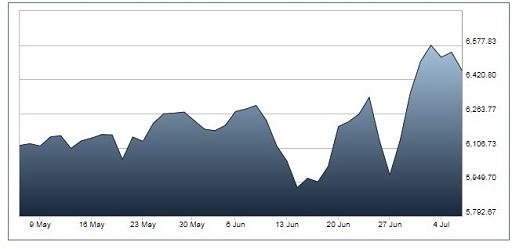

1.4.3 Why did the FTSE 100 behave like a rollercoaster in 2016?

There is no equation that formally links the factors set out in the previous section with the performance of share prices – at best, there are strong correlations at work. Yet all the major swings in equity prices seen in recent decades can be explained by the economic contexts defined by these factors.

Let’s try a recent episode out to test the theory!

Activity 1.4 FTSE 100

Have a look at the graph in Figure 18. It shows the movements in the UK’s leading share index, the FTSE 100, between May and July 2016.

Clearly this was a period of share price volatility with the index falling sharply in June only to stage a very strong recovery into July.

This period saw unremarkable activity in the economy with inflation and interest rates low and with economic growth steady.

So what caused the volatility and what led to investor sentiment first turning negative and then, very quickly, becoming positive?

Here’s a hint: referendum.

Discussion

The key driver of the volatility in the FTSE 100 was the referendum on the UK’s membership of the European Union (EU). This took place on 23 June 2016 and resulted in a vote for the UK to leave, with 52% voting for an exit versus 48% voting to stay in the EU. This was an outcome that was not expected by the opinion polls and hence it was a major ‘surprise’ to the public and the financial markets.

Ahead of referendum day the volatility in the FTSE 100 index reflected swings in the opinion polls but the actual result initially led to share prices, taking the index down in the process. The reason for the initial negative reaction was that the outcome was taken to be ‘bad news’ – at least in the medium-term – for the economy (although the actual impact of leaving the EU on the UK economy will only be known in the years after ‘Brexit’).

Within days, though, investor sentiment changed. This was because investors realised that many of the companies that comprise the FTSE 100 earn a significant (or, indeed, a major) proportion of their earnings in overseas (non-UK) economies. These overseas economies are not going to be directly affected by Brexit.

Additionally the vote to leave the EU led to a sharp fall in the value of the UK pound. This fall was forecast to have beneficial effects for many FTSE 100 companies since:

- the sterling value of overseas earnings (e.g. in US dollars) by FTSE 100 companies is increased

- those companies producing goods and services in the UK for export overseas would find it easier to sell them due to the fall in the value of the pound

- UK consumers, faced with a lower value for the pound, would be less likely to buy goods from overseas companies and would divert spending to UK companies.

So the initial adverse response of investors was quickly turned round as careful analysis replaced emotional sentiment in the assessment of the prospects for the FTSE 100 companies.

Brexit may be bad for many parts of the economy but this does not necessarily mean it is bad news for the FTSE 100. This index is a collective measure of the financial health of the 100 biggest companies listed on the London Stock Exchange – many of whom obtain a large portion of their earnings from overseas sales. The index is, therefore, not a wholly reliable measure of the overall health of the UK economy.

1.5 Week 1 quiz

Check what you’ve learned this week by taking the end-of-week quiz.

Open the quiz in a new window or tab then come back here when you’re done.

Week 1 round-up

It has been a very full first week and you will have learned much about the need for effective investment planning and some of the initial building blocks for your strategy.

You looked at why investing for the future is essential for households – particularly in the light of the evidence that we, in the UK, aren’t doing enough to save for the future.

You looked at the first things you need to consider when devising your investment plan and at the importance of the time horizon for your investments and the future spending plans that your investments will support.

You then looked at the drivers of two key determinants of investment returns – interest rates and equity markets.

Next week, you’ll start to examine in detail the characteristics of the spectrum of investment products available for you to employ within your investment strategy.

You can now got to Week 2 .

Images

This course was written by Martin Upton.

Except for third party materials and otherwise stated in the acknowledgements section, this content is made available under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 Licence .

The material acknowledged below is Proprietary and used under licence (not subject to Creative Commons Licence). Grateful acknowledgement is made to the following sources for permission to reproduce material in this course:

Figure 2 © Metro-Goldwyn-Mayer via Getty Images

Figure 11 © MachineHeadz, LifesizeImages via iStockphoto.com

Figure 16 © Carl Court via Getty Images

1.2.7: PUFin www.open.ac.uk/ pufin © The Open University

1.3.3 compilation video contains © BBC archive

1.4.1 from Radio 5’s Wake up to Money Programme © BBC

Every effort has been made to contact copyright owners. If any have been inadvertently overlooked, the publishers will be pleased to make the necessary arrangements at the first opportunity.

Don't miss out:

1. Join over 200,000 students, currently studying with The Open University – http://www.open.ac.uk/ choose/ ou/ open-content

2. Enjoyed this? Find out more about this topic or browse all our free course materials on OpenLearn – http://www.open.edu/ openlearn/

3. Outside the UK? We have students in over a hundred countries studying online qualifications – http://www.openuniversity.edu/ – including an MBA at our triple accredited Business School.

References

Bank of England (2023) Official Bank Rate History [online] Available at https://www.bankofengland.co.uk/ boeapps/ database/ Bank-Rate.asp (Accessed 10 October 2023)

Department for Work and Pensions (DWP) (2020) Family Resources Survey 2018/19 (savings and investments data tables) [online], https://www.gov.uk/government/statistics/family-resources-survey-financial-year-201819 (Accessed 24 November 2020)

Department for Work and Pensions (DWP) (2023) Family Resources Survey: financial year 2021 to 2022, Tables 7.1 and 7.9. [online] Available at: https://www.gov.uk/ government/ collections/ family-resources-survey--2 (Accessed 10 October 2023)

London Stock Exchange (LSE) (2017) ‘FTSE-100 Interactive Graph’ [Online]. Available at http://www.londonstockexchange.com/exchange/prices-and-markets/stocks/indices/summary/summary-indices-chart.html?index=UKX (Accessed 5 December 2017).

Nationwide (2023) Annual percentage change in UK house prices [online] Available at https://www.nationwidehousepriceindex.co.uk/ resources/ f/ uk-data-series (Accessed 10 October 2023)

Office for National Statistics (ONS) (2023a) Households’ saving ratio (per cent) [online] Available at https://www.ons.gov.uk/ economy/ grossdomesticproductgdp/ timeseries/ dgd8/ ukea (Accessed 10 October 2023)

Office for National Statistics (ONS) (2023b) RPI All Items: Percentage change over 12 months: Jan 1987 = 100 [online] Available at https://www.ons.gov.uk/ economy/ inflationandpriceindices/ timeseries/ czbh/ mm23 (Accessed 10 October 2023)

‘Organisation for Economic Co-operation and Development (OECD) (2023) Household savings. [online] Available at https://data.oecd.org/ hha/ household-savings.htm. Accessed 10 October 2023’