3.1.2 The accounting equation

The financial position of a business is expressed in the statement of financial position, which is more commonly called the balance sheet. The financial position of a business is represented by:

- assets (what the business owns)

- liabilities (what the business owes)

- owner’s capital (the monetary value of the owner’s investment in the business).

As you may remember from Week 2, the accounting equation (also called balance sheet equation), for any business, says:

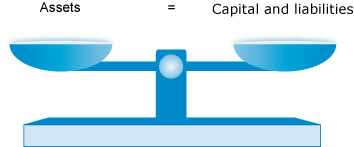

| Assets = Capital + Liabilities |

Figure 1 below demonstrates the accounting equation.

The accounting equation should be kept in balance at all times i.e. the assets on the left side of the equal sign should always be the same as the sum of the capital and liabilities on the right-hand side.

Activity 1 The relationship between assets, liabilities and capital

A business at the end of its first year of trading has assets of £10,000 and liabilities of £8,000.

- What is the capital position of the business at the end of its first year?

Answer

£2,000

Show the position of the business according to the accounting equation.

Answer

Assets of £10,000 = Capital of £2,000 + Liabilities of £8,000

Any change in assets, capital or liabilities in the business has to keep the accounting equation in balance. If, for example, the business buys goods for sale for £200 on credit from a supplier then the accounting equation will look as follows:

Assets of £10,000 + £200 (new asset) = Capital of £2,000 + Liabilities of £8,000 + £200 (new liability)

or £10,200 = £2,000 + £8,200

This increase in both assets and liabilities in this example is known as the dual effect of every transaction. The next activity will help you to understand this better.

Activity 2 The dual effect of any transaction

A business buys a printer for £80 from the cash it keeps available for all expenditure under £100.

- What is the dual effect of this transaction?

Answer

The asset printer increases by £80 and the asset cash decreases by £80.

- What is the effect on the accounting equation of this transaction?

Answer

The accounting equation of the business will stay the same as the figure for assets will stay the same i.e. £80 - £80 = £0.

In the next section, the dual effect – also known as the duality principle – of every transaction will be looked at in more detail.