Use 'Print preview' to check the number of pages and printer settings.

Print functionality varies between browsers.

Printable page generated Friday, 24 July 2026, 4:05 AM

Sources of funding

Introduction

Have you ever thought, ‘Where does the money come from that I need to start and grow my business?’ Many start-up entrepreneurs face this challenge. To help you understand the role of money in entrepreneurship, this unit focuses on funding and the fundamentals of cash flow management to get you started.

Young and innovative entrepreneurial businesses help create, develop and grow new technologies, industries and markets and provide solutions to pertinent societal challenges. Yet, these businesses need considerable amounts of financial resources to get started, grow and succeed. Considering the importance of entrepreneurship for the overall economic system, there is a need for a better understanding of distinct sources and types of funding, and of how those sources of funding can be used by start-ups and how they affect the growth and sustainability of new ventures.

This unit offers you an overview on funding strategies, cash flow management to sustain the growth of the venture, and traditional and new sources of funding, as well as grants provided by the UK government and regional initiatives.

By the end of this unit you will be able to evaluate the pros and cons of different means of funding and support for your venture.

1 Funding strategies

How business start-ups are financed is one of the most important questions in entrepreneurship. The first thing that you will learn as a start-up entrepreneur is that not all money is the same. As Burns (2016, p. 359) puts it, ‘Different sorts of money ought to be used for different purposes and not all types of money are available to all new ventures.’

Table 1 depicts the main types of financial capital and how they should be used. Generally, the term duration of the source of finance should fit with the term duration of the use to which the money is put. That means that fixed or permanent assets should be financed by long- or medium-term sources of finance. Short-term finance, such as an overdraft, serves the purpose of mitigating fluctuations in working capital.

| Duration of finance | Source of finance | Use of finance |

|---|---|---|

| Long- and medium-term |

|

|

| Short-term |

|

Seasonal fluctuations in working capital: stock, debtors (net creditors) |

In practice, start-up entrepreneurs rely on a combination of various inflows of money. These are broadly classified by source (formal or informal) and by type (debt or equity).

As it is easily available at short notice, start-up entrepreneurs often try to fund their new business with their own money, typically coming from savings and borrowing, secure on a property or unsecure on a personal guarantee. Credit cards are an easily accessible and flexible source of funding, albeit an expensive one.

Having exhausted their personal capital, many entrepreneurs borrow money from friends and family members – i.e. bootstrapping. These informal investors often require lower returns than formal investors such as venture capitalists and business angels. Relatives and friends are even approached before founders ask banks for loans.

However, informal sources of funding are not unlimited. For sustainable growth, entrepreneurs need to turn to more formal sources of funding, either by borrowing money from banks, i.e. loans, or by raising equity from formal investors (Blundel et al., 2017).

The purchase of fixed assets can also be financed by lease. Having a lease allows the firm to use an asset without owning it. They can make regular lease or hire purchase payments, which allows the firm to purchase the asset over a period of time, and the asset can be used as security in the event of default (Burns, 2016).

Crowdfunding is a novel source of funding. It allows individual investors to support new ventures with relatively small contributions and is typically via online platforms. Crowdfunding can take the form of equity investment and loan capital, debt finance or peer-to-peer lending (Blundel et al., 2017).

Most start-up entrepreneurs find it challenging to conceive of an appropriate funding strategy and to decide on sources and types of funding. The flowchart in Figure 1 guides you through the process of deciding what type and source of funding is most appropriate and available to you.

Activity 1 Designing your personal funding strategy

Use the flowchart depicted in Figure 1 to help you plan a funding strategy for your new venture.

Reflect on the constraints and obstacles in getting access to the financial capital that you identify in the process. What opportunities do you see to overcome them?

Discussion

Everyone’s circumstances are different but you might have thought of the following constraints and obstacles:

Lack of awareness of opportunities to apply for a grant

No money available from family or friends

Lack of personal savings

Difficulties in attracting co-founders

Personal circumstances, such as age, health and family situations, family and work commitments

Lack of knowledge in business and management.

Opportunities to overcome obstacles include, but are not limited to, seeking advice from experts in finance and/or entrepreneurship, applying for support from a business incubator or an accelerator, and joining networks of like-minded start-up entrepreneurs.

2 Cash flow management

Every entrepreneur needs to think about money – making money, investing money, spending money, having enough money to pay the bills. But have you ever asked yourself, ‘What is money?’ Sometimes it appears to be so important that you could be forgiven for thinking that money is all that entrepreneurship is about. Of course, entrepreneurship means many more things and money is only one of them.

About two-thirds of small businesses face money problems. Reasons for these problems are, for example:

difficulties in collecting money due from customers

seasonal variations in sales

critical incidents, such as increasing prices for raw materials or an unexpected decrease in sales.

All enterprises have different cash-to-cash or operating cycles; i.e. the time it takes for a business to access capital and resources, produce and sell its goods and services, and collect cash from sales. Depending on the type of business, the cycle can take just a few hours or up to several years.

Many small businesses fail because they underestimate the time lag between receiving cash and spending cash, or they experience a mismatch between the size of payments received and the size of payments that must be made (Burns, 2016). To avoid these problems you need to understand the flows of money that come in and go out, chiefly the basics of managing cash flow.

Cash can come from three different sources:

Operations, which includes the sales of goods and services that you produce, and collecting cash from customers.

Investing, which comprises buying and selling shares, bonds, land, buildings and equipment.

Financing, which means either cash given to the business in return for ownership (i.e. equity) or money borrowed from other sources, such as banks.

To understand the inflow and outflow of money, watch the following video, Financial Statements Explained in One Minute: Balance Sheet, Income Statement, Cash Flow Statement.

The video introduced three important documents that you need for your cash flow management:

the balance sheet, which reflects your past operations and the net worth (equity) of your enterprise

the profit and loss statement, which is sometimes referred to as an income statement and thus shows how profitable your enterprise is

the cash flow statement, which shows the inflow and outflow of your money and thus indicates how credible your profit numbers in the profit and loss statement are.

2.1 Profit and loss statement

A profit and loss statement indicates the relationship between sales (revenue or turnover), cost of sales, gross profit, operating expenses, interest, tax and net profit for a specific period of time. It provides useful information for founders, shareholders, providers of capital and staff. A profit and loss statement is usually prepared annually.

As shown in Table 2, the profit and loss statement reveals revenues and costs and how much profit has been made over a particular period (Blundel et al., 2017).

| PROFIT AND LOSS STATEMENT for the year ended 31 December 2016 | ||

|---|---|---|

| Income | £ | £ |

| Sales | 6,600,000 | |

| Stock at 1 January 2016 | 700,000 | |

| Purchases | 4,900,000 | |

| 5,600,000 | ||

| Stock at 31 December 2016 | (980,000) | |

| 4,620,000 | ||

| Gross Profit | 1,980,000 | |

| Profit Margin | 30.0% | |

| Expenditure | ||

| Establishment expenses | 160,000 | |

| Administration | 370,000 | |

| Selling and distribution expenses | 1,200,000 | |

| Finance charges | 20,000 | |

| Total operating expenses | 1,750,000 | |

| Operating profit | 230,000 | |

| Net interest | 30,000 | |

| 30,000 | ||

| Net profit before taxation | 200,000 | |

| Net margin | 3.0% | |

| Tax | 40,000 | |

| Dividends | 10,000 | |

| 50,000 | ||

| Net profit retained | 150,000 | |

A profit and loss statement includes:

Income (generated by business activities but not interest received)

Cost of sales (cost of purchased goods and manufactured goods, including manufacturing overheads and wages)

Gross profit (income less cost of goods)

Profit margin (gross profit / income x 100)

Operating expenses (overhead and staff, excluding wages for manufacturing)

Depreciation

Operating profit (gross profit less operating expenses)

Interest

Net profit (gross profit less operating expenses and interest)

Net profit before tax

Net margin (net profit before tax / income x 100)

Corporation tax

Net profit after taxes.

Every start-up entrepreneur needs to know how to prepare a profit and loss statement. Consider that, for a start-up, it is important to complete this statement on a monthly basis for at least the first two years. This enables you to spot trends. Activity 2 will help you to prepare a profit and loss statement for your own business.

Activity 2 Preparing a profit and loss statement

Use the example shown in Table 2 as a guide to produce a profit and loss statement for your own venture. It should reflect the projected results of the operation for a given period of time.

Discussion

Did you find this exercise easy or difficult to do? Are there still parts of the profit and loss statement that you don’t fully understand? For example, you might not be sure about how high your tax burden will be. Depreciation is also an issue. For tax purposes, you may deduct the cost of the tangible assets you purchase as business expenses. Thereby, you must follow the national tax laws about how and when you may take the deduction. A conversation with a tax advisor might be useful.

These examples reveal that you should consider each line of your profit and loss statement thoroughly and reflect on what the numbers mean to your business. The net profit retained will not only be used for the assessment of how profitable your business is, it will also be included in your balance sheet.

2.2 Balance sheet

Unlike the profit and loss statement, which focuses on a specific period of time, the balance sheet is a projection of assets, liabilities and equity at a specific point in time. As depicted in Table 3, the balance sheet summarises the financial situation of the business at, for example, a month end or the year end. The net worth must equal assets minus liabilities and ownership equity.

| SUMMARY BALANCE SHEET as at 31 December 2016 | ||

|---|---|---|

| £ | £ | |

| Fixed assets | ||

| Tangible assets | 45,000 | |

| Investments | 20,000 | |

| 65,000 | ||

| Current assets | ||

| Stocks | 980,000 | |

| Debtors | 1,410,000 | |

| Cash at bank and in hand | 110,000 | |

| 2,500,000 | ||

| Total assets | 2,565,000 | |

| Creditors: amounts falling due within a year | (2,200,000) | |

| Net current liabilities | 300,000 | |

| Total assets less current liabilities | 365,000 | |

| Capital and reserves | ||

| Owners share capital | 1,000 | |

| Profit and loss account, including £150,000 for | ||

| year end 31 Dec 2016 | 364,000 | |

| 365,000 | ||

Let’s turn to assets first. The first area to look out for is fixed assets. These include things like computers, furniture, stock and other physical items. Current assets – also referred to as short-term assets – comprise things such as cash in the bank and in hand, money in the till and anything you are owed (i.e. your debtors). In contrast to fixed assets, current assets can include any assets that will be converted into cash within one year from the date shown in the heading of the company’s balance sheet.

Now let’s turn to liabilities – the amount that your business owes to other entities. Creditors means the amount of money you must pay out over the coming year, such as office lease and loan repayments. Accrued liabilities are expenses incurred but not paid for, such as products, services and wages. Liabilities also include tax owed, such as company tax and employment-related taxes that need to be paid within a given timeframe.

The Financial Statements Explained in One Minute video introduced the notions of assets (such as cash in the bank, inventory or real estate) and liabilities (such as debt to suppliers). Subtracting liabilities from assets shows you the net worth (or equity) of your business.

Going beyond the video, you can consider the working capital. For this purpose, you may have a look at Table 3. The working capital is the difference between current assets (such as cash, accounts receivable (i.e. customers’ unpaid bills) and inventories of raw materials and finished goods) and current liabilities (such as accounts payable).

The net worth (or owner’s equity, sometimes also referred to as net assets) is calculated from the total assets minus the total liabilities. It includes the share capital and retained profit or loss. If this figure is positive then the business is financially healthy. If it is negative the business is insolvent and extra funds are needed (Blundel et al., 2017).

Activity 3 will help you to prepare a balance sheet for your own business and reflect on its financial health.

Activity 3 Preparing a balance sheet

Produce a balance sheet that projects your business’s assets, liabilities and owner’s equity at a specific point in time. Use the sample balance sheet shown in Table 3 to help you.

Looking at your balance sheet, is your business financially healthy?

Discussion

Did you find this exercise easy or difficult to do? Are there still elements of the balance sheet that you don’t fully understand?

As a starting point, you should have used any available numbers referring to your own business and inserted them into an Excel spreadsheet that looks like Table 3. The video has shown how you can calculate the net worth (or equity) of your enterprise. This provides a snapshot of your business. Using the notion of working capital, you can gain even more insights into the financial health of your business.

2.3 Cash flow statement

The final set of financial statements are projected cash flows. A cash flow statement is usually prepared last because it includes data from its corresponding profit and loss statement and balance sheet (Barringer, 2015).

Both statements provide vital management information, but neither tells us anything about how much money is flowing in and out of the business.

The Financial Statements Explained in One Minute video illustrated that producing, analysing and interpreting cash flow is important for assessing the credibility of your profit and loss statement. But what exactly does this mean?

The basic idea behind a cash flow statement is to start with a beginning balance, like the amount of cash you have on hand at the beginning of a month; add your projected monthly income (or loss); and then list all the other transactions that either add or subtract from your cash.

Typically, your cash flow statement (Table 4) should be divided into the balance brought forward from the previous period, the income that your business generates, the expenditure that you have for running your business, and the resulting balance that is carried forward to the next period.

| Week no. | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

|---|---|---|---|---|---|---|---|---|

| Balance brought forward | ||||||||

| Income | ||||||||

| Expenditure | ||||||||

| Balance carried forward |

Activity 4 will help you to prepare a cash flow statement for your own venture.

Activity 4 Preparing a cash flow statement

Produce a cash flow statement for your start-up, using the example in Table 4 as a guide.

Reflect on the numbers that you see and think carefully about whether your venture will be able to maintain a sufficient cash balance to run successfully.

Discussion

Did you find this exercise easy or difficult to do? Are there still elements of the cash flow statement that you don’t fully understand?

If so, you might reflect on the reasons for this. It is possible that you cannot easily forecast any inflows and outflows of money. Making predictions about future sales, for example, requires some market research and a good understanding of the customers that you aim to serve.

Similarly, you might not be fully aware yet of the expenditure that you will have to cover. For example, there may be an unexpected increase in the rent for your warehouse or you may not have fully considered the insurances that you might need for running your business.

3 Alternative sources of funding

Getting the money to start or grow a business seems like one of the greatest challenges, but in reality most people who try find the means to get their business going. There are two reasons for this. First, financing is often easier than people think, because most of us have many assets and financial resources that we take for granted. Second, the range of financing resources available to us is so varied that few people just starting out in business know more than a fraction of the options available to them.

3.1 Borrowing

When you decide to finance your venture with debt, where can you get access to loans to start and grow your business?

As you might expect, your best source is the bank where you are currently doing business. After all, it is in the business of making loans. You are a customer. As such, you are a known commodity – you pay your bills, you keep your account balance positive, you don’t bounce checks. Start where you’re known.

Nonetheless, the choice of the right bank can be challenging. It takes some time to find the right bank and establish a trusting business relationship with it (Blundel et al., 2017).

Usually, banks do not take a shareholding or have an interest in the business. Therefore, any capital needs to be repaid after a contractually agreed duration, and interest is charged either at a variable rate (base rate plus a fixed amount) or a fixed rate.

It is important to remember that the bank assesses the risk and their return when calculating rates and each bank will have different policies on this. Banks will normally charge a fee for arranging financing and annually for agreeing overdrafts.

Generally, we distinguish between unsecured and secured borrowing. Credit card debt is a widely used form of unsecured borrowing. Although it is more expensive than other formal borrowing, credit card debt is very popular among entrepreneurs. This is because a credit card is easier to use and to get access to than bank borrowing. A credit card can streamline payments and is an anonymous form of funding that does not require any explanation to the lender.

Trading activities are often funded by an overdraft linked to a current bank account. Using an overdraft means borrowing at a variable interest rate, with a limit that is typically agreed each year and for an arrangement fee. This flexible type of unsecured borrowing is suitable for day-to-day expenses, but it can lead to high fees if the overdraft limit is exceeded (Blundel et al., 2017).

Loans are a form of secured borrowing. The entrepreneur (i.e. the borrower) incurs a debt and must pay interest on that debt until it is repaid to the bank (i.e. the lender) within a given period. The interest serves as an incentive for the bank to provide the loan. Interest rates can be subject to change and renegotiation (Blundel et al., 2017).

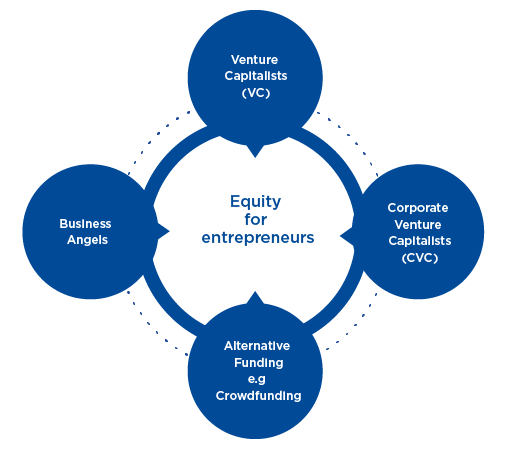

3.2 Equity

The modern entrepreneurial equity funding landscape generally comprises four sources: venture capitalists (VC); corporate venture capitalists (CVC); business angels and alternative sources of equity funding (Figure 2).

Venture capitalists

Although venture capitalists tend to fund only a small number of start-ups, in practice they represent the most recognised form of equity financing (especially for businesses with a high growth potential). Venture capitalists usually raise funds from a network of partners, such as university endowments or pension funds, and aim to provide a return to these investors through selective investments in young, innovative start-ups.

Venture capitalist firms often collaborate closely with the businesses in which they invest. Entrepreneurs benefit from the guidance and advice that VCs provide. The typical planning horizon of a VC is about ten years. Within this period of time investors expect a return from their investments. At the end of the funding period, VCs often exit via an acquisition or initial public offering (IPO) (Drover et al., 2017).

Corporate venture capitalists

Corporate venture capital means that an established corporation makes an equity investment in a start-up. This type of funding differs from traditional venture capital because the funding is provided by dedicated units of corporations. These units go beyond the primary purpose of their parent companies (Drover et al., 2017).

Business angels

Business angels are individual investors who invest their own money in promising early-stage start-ups. They are often former entrepreneurs, who aim to use their knowledge and experience in their area of expertise to help other entrepreneurs to start and grow a new business.

Recently, business angels have become more formalised by setting up networks of angel investors (Drover et al., 2017). A list of UK-based business angel networks can be found at syndicateroom.com.

While some angel networks invest globally (for example, Angel Investment Network), others focus on selected geographical areas (for example, London- and Cambridge-based Cambridge Angels and Minerva Business Angel Network focus on the East Midlands, Thames Valley, West Midlands and Yorkshire).

Alternative funding

Novel sources of funding are emerging. Among them, crowdfunding and accelerators (or incubators) have become most popular.

Crowdfunding or crowdsourcing is a relatively new form of business financing that allows individuals to support new ventures with small contributions and typically online. Globally by 2016, it was estimated that $34 billion was made available through crowdfunding sites.

Two crowdfunding platforms are, for example, crowdfunder.com and crowdcube.com.

Accelerators or incubators are cohort-based programmes, which provide a combination of mentorship, work space and funding to early-stage start-up entrepreneurs in exchange for equity. One business that used accelerator funding is:

AirBnB, the famous website for finding short-term accommodation. AirBnB was founded in 2008. The following year, the venture was admitted to the incubator program of Ycombinator. During the three months of incubation, important strategic changes were implemented, including the change of name from Airbedandbreakfast.com to AirBnB.com. In the years following the program, the venture raised a total of $2.39B from prominent angel investors such as movie star Ashton Kutcher, as well as VCs such as Sequoia, Andreessen Horowitz, and Greylock Partners.

Most accelerators are associated with universities. Entrepreneurs usually apply for an opportunity to develop a business idea on site during a fixed period of time (usually three to six months). At the end of this period, cohorts of start-up entrepreneurs benefit from a ‘demo day’, where they can present and pitch their business ideas to potential investors (Drover et al., 2017; Katz and Green, 2014).

4 Grants and initiatives

Grants and regional and national initiatives are an increasingly important source of early-stage financing.

Using small business grants can be extremely appealing. After all, it’s money you don’t have to pay back, which means no interest payments, no late payments and no chance of losing any collateral. So, why doesn’t every small business owner forego a small business loan and take advantage of this free money?

This is easier said than done.

First, to get access to a grant, you must search for and find a grant you would be eligible for. This search and selection process requires some personal investments in time and effort.

Second, when you apply for a grant, you will compete with other businesses for the same money. Thus, you must prepare a strong and persuasive application and know any criteria, guidelines and deadlines very well.

Third, if your application is successful, you will have to adhere to clear instructions on how and when you may use the money and for which purposes. In regular reports you will have to demonstrate that you use the grant effectively, and your business may be used to showcase the activities of the initiative providing your grant.

4.1 Finding a grant

There are several opportunities for you to identify grants that suit you. Sometimes, an exploratory Google search can provide some initial information. You can also ask family and friends or experienced entrepreneurs for advice. Entrepreneurship fairs, such as the Business Startup Show, are a good occasion to meet successful entrepreneurs and learn from their experiences.

Social media platforms are also useful. For example, you can join the Santander LinkedIn group. Santander also provides entrepreneurship and enterprise support through a dedicated support website.

4.2 National and regional initiatives

Schemes for businesses that are not yet trading, or are in the start-up stage, can be found on the Department for Business, Energy & Industrial Strategy’s website. The Entrepreneur Handbook showcases a list of funding opportunities especially for small businesses.

If your business is located in Northern Ireland, you can have a look at the Northern Ireland Business Support Finder, a database that you can search for opportunities for publicly funded support. Also look at Invest NI, the regional business development agency.

Grants are available for diverse types of business, such as:

food and drink businesses (Food Enterprise Advisory Support Team (FEAST) – East Midlands)

rural businesses (LEADing Rural Business Programme in Bedfordshire, the Chilterns and Clay Vales, Greensand Ridge, Huntingdonshire and Worcestershire)

small tourism companies in the district of Eden

renewable energy suppliers (LCR Future Energy).

The grants address various purposes, among them cultural and social issues. See, for example:

Heritage Enterprise (HE) – UK – a scheme dedicated to helping community organisations across the UK restore neglected historic buildings and sites and unlock their economic potential.

Key Fund – Midlands and the North of England – a scheme aiming to provide grants and loans to social enterprises in the specified region to increase their community and economic and environmental impact.

A large number of grants represent regional initiatives. Examples include (but are not limited to):

Grants for business growth – Stoke-on-Trent and Staffordshire – aims to support small- to medium-sized businesses (SMEs) in this region that have been trading for more than twelve months and have a project costing at least £40,000.

- Future Focus and the Isles of Scilly provides small grants of up to £2,500 to purchase equipment and resources, access research and knowledge, and subsidise salary costs for new employees or support innovation projects started by existing employees.

South East Midlands Start-up Programme (part-funded by the European Development Fund) – offers access to free business start-up support to residents in Aylesbury Vale, Bedfordshire, Central Bedfordshire, Cherwell, Corby, Daventry, Milton Keynes, Northampton, Thrapston and Wellingborough.

Other grants are national initiatives:

Innovate UK is a case in point. It aims to nurture the establishment of technology start-ups and helps them apply their innovative ideas to commercial ends.

The Gigabit Broadband Voucher Scheme (GBVS) – UK provides grants for SMEs in England, Scotland, Wales and Northern Ireland that aim to upgrade business broadband to a high-speed capable connection.

CRACK IT Challenges targets industry, academics and SMEs in the UK that are interested in taking part in a challenge-led competition and in working together to solve business and scientific challenges, such as the development of new technologies and their application to commercial ends and the use of animals for scientific purposes.

The Prince’s Trust grants are suitable for young entrepreneurs (aged 18–30 years) who are seeking advice, mentorship and small amounts of money (individual grants: £1,500; business groups: up to £3,000) to start a business.

Activity 5 Searching for a grant

Summary

In this unit you have reflected on funding. You have considered the importance of funding and how you can raise funds to start your own business. You have also begun to consider the pros and cons of different sources of funding, the uses of different types of funding, and why it is important to have effective cash flow management.

You have learned:

the meaning of the term ‘funding’

the opportunities you have to get access to different sources and types of funding for starting a new venture and making it prosper

the importance of cash flow management

how to find and select a grant.

Congratulations on completing the unit Sources of funding. We very much hope that you have enjoyed the unit and that the learning experience proves useful and rewarding to you in the future.

References

Acknowledgements

Every effort has been made to contact copyright holders. If any have been inadvertently overlooked the publishers will be pleased to make the necessary arrangements at the first opportunity.

Important: *** against any of the acknowledgements below means that the wording has been dictated by the rights holder/publisher, and cannot be changed.

Grateful acknowledgement is made to the following source:

Figure 1: Burns, P. (2016) Entrepreneurship and Small Business. Start-up, Growth and Maturity (4th ed.), Palgrave.