Use 'Print preview' to check the number of pages and printer settings.

Print functionality varies between browsers.

Printable page generated Sunday, 26 July 2026, 7:19 AM

Session 2: Earning and spending money

Learning outcomes

Session learning outcomes

Session learning outcomes

By completing this session, you will be able to describe:

The importance of financial planning.

How to prepare simple budgets.

Glossary

Glossary

2.1 Earning money

Money enables people to buy or sell goods (like mobile phones or ice creams) or services (like holidays or gym memberships). Most people earn money by working for others or by running their own business.

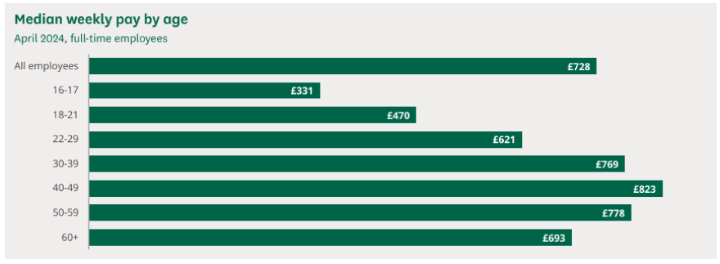

The amount of money that people earn usually changes with their age.

The graph below shows the weekly pay of a typical (median) person in different age groups. The graph shows that a typical (median) 16–17-year-old young adult earns around £331 (before tax) per week (Office for National Statistics, 2024).

Something to talk about – which occupation will you choose?

Something to talk about – which occupation will you choose?

There are many factors that affect people’s occupational choices.

One factor is the amount of money that different occupations offer.

1. Use this interactive tool by the Office for National Statistics to explore annual income (before tax) for different occupations.

2. Which occupation might you choose after you finish your education or training?

Feedback

The question related to your occupational choice is a difficult one. So, please do not worry if you do not yet know the answer.

Looking at income for different occupations may give you an idea about what you would like to do.

However, please do keep in mind that money is not the only thing that affects the occupations that people choose.

People choose occupations depending on what they love doing. Their occupational choice also depends on the opportunities available in the economy.

At this stage of your life, keep learning and exploring!

2.2 Is financial planning important?

Financial planning usually requires the following.

Clear financial goals. |

Accurate and timely budgeting. |

Appropriate savings and investment strategies. |

A sensible retirement plan. |

As you move into your professional lives, you should start thinking about preparing a careful financial plan.

However, as a young adult, it is unlikely that you will prepare an elaborate financial plan with detailed investment and retirement long-term financial goals.

Still, getting into the habit of simple financial planning early could be beneficial for the following reasons.

Click on each number to learn more.

Something to talk about – does financial education work?

Do you think financial education makes a difference to financial behaviour of young people?

Feedback

A study by the Money and Pension Service (MaPS) suggests that young people who receive financial education “feel more confident about managing their money” and “save money more regularly” than those who do not (MaPS, 2023).

If you'd like to learn more, this is the study: UK Children and Young People’s Financial Wellbeing Survey: Financial Foundations | Money and Pensions Service.

2.3 How do I start financial planning?

You do not need an elaborate financial plan that captures your investments and retirement goals.

Instead, you can start by setting simple financial goals such as saving money for a new book or for a new laptop.

You may also think about bigger goals like saving money for a holiday after you finish at school or for starting your own business.

The key idea is to spend a few minutes thinking about what financial goals you would like to achieve in the near future.

Setting financial goals

Use the box below (or write down in your notepad) to make a short list of financial goals that are important to you.

Feedback

Setting financial goals (or any other goals) takes time. So, do not worry if you cannot think of the best financial goals.

Just start with a list of possible goals. Do not hesitate to write bigger financial goals. For example, your goal may be to save to buy your own house or start your own business. After all, there are many examples of young teenage entrepreneurs who started planning quite early in life.

You can come back to your list in the future and revise it as you learn more about your spending habits, your income and your future opportunities.

2.4 Budgeting

The basic idea behind budgeting is to keep track of the money that you receive and the money you spend.

The goal of budgeting is to make the best use of your money and, to the extent possible, save some money for the future.

Two monthly budgets of a young adult are shown in the tables below. This young adult has a simple financial goal: Save at least £5 every month.

| Money received: | Amount (£) | Money spent: | Amount (£) |

|---|---|---|---|

| Pocket money | £32 | Book purchase | £7.99 |

Money from work (Gardening) | £7 | Eating out with friends | £11.65 |

| Birthday present | £25 | Mobile phone top-up | £6.99 |

| Birthday present | £12 | ||

| Clothes (new shirt) | £19.99 | ||

| Total | £64 | Total | £58.62 |

| Monthly surplus | £64 - £58.62 = £5.38 |

| Money received: | Amount (£) | Money spent: | Amount (£) |

|---|---|---|---|

| Pocket money | £27 | Cinema | £5.99 |

Money from work (car wash and gardening) | £11 | Mobile phone top-up | £6.99 |

| Sale of old clothes | £10 | Eating out with friends | £23.64 |

| New mobile phone case | £6.99 | ||

| Sweets | £2.50 | ||

| Total | £48 | Total | £46.11 |

| Monthly surplus | £48 - £46.11 = £1.89 |

Preparing your own budget

After reading the two example budgets, prepare your own budget for next month based on the money that you received and spent in the past 30 days.

Use the box below (or write down in your notepad) to make notes.

Feedback

You may not remember all the money that you received or spent. You can create a list of categories for Money received on the left-hand side, and another list for Money spent on the right-hand side.

This rough budget may help you to create a more detailed and accurate budget for the next month. It may also enable you to decide how much you are willing and able to save.

There are several mobile phone apps that may help you create your budget.

You will learn about bank accounts in the next session.

Moving on

References

Money & Pension Service (MaPS) (2023) UK Children and Young People’s Financial Wellbeing Survey: Financial Foundations | Money and Pensions Service. Available at: https://maps.org.uk/en/publications/research/2023/uk-children-and-young-peoples-financial-wellbeing-survey-financial-foundations (Accessed 16 July 2025).

Office for National Statistics (2024) 'Average earnings by age and region', House of Commons Library, UK Parliament. Available at https://commonslibrary.parliament.uk/research-briefings/cbp-8456/ (Accessed 16 July 2025).

Acknowledgements

Grateful acknowledgement is made to the following sources:

Every effort has been made to contact copyright holders. If any have been inadvertently overlooked the publishers will be pleased to make the necessary arrangements at the first opportunity.

Important: *** against any of the acknowledgements below means that the wording has been dictated by the rights holder/publisher, and cannot be changed.

Images:

565845 : Image: People thinking about expenses : mentalmind / Shutterstock

565846 : Image: Woman working from home : mentalmind / Shutterstock

565847: Image: Piggy bank growth chart: eamesBot / Shutterstock

565848: Image: Budgeting pie chart: Buravleva stock / Shutterstock

565896: Image: Paper plane: Wirestock Creators / Shutterstock

2.1 Earning money - ONS, Annual Survey of Hours and Earnings, 2024 chart