Week 1: Financial planning and the life course

Use 'Print preview' to check the number of pages and printer settings.

Print functionality varies between browsers.

Printable page generated Saturday, 20 June 2026, 11:41 AM

Week 1: Financial planning and the life course

Introduction

Before you start, The Open University would really appreciate a few minutes of your time to tell us about yourself and your expectations of the course. Your input will help to further improve the online learning experience. If you’d like to help, and if you haven't done so already, please fill in this optional survey.

Martin Upton is your educator and guide through the course. He is Director of the True Potential Centre for the Public Understanding of Finance, based at The Open University Business School. He’ll meet you at the start of each week of the course to tip you off about highlights and challenges, to remind you of what you’ve learned and to help you make the most of Managing my money. Note that each of the eight weeks of the course is designed to be studied over a period of three hours, ideally with one week being studied per week.

Transcript

As the course progresses you’ll also meet personal finance expert Jonquil Lowe from The Open University.

Your financial profile

Some of the coolest features are the financial challenges, planners and calculators you get to explore throughout the course. See how you score in the financial bad habits test, build up your personal budget and household balance sheet, and develop your own ‘fact find’ to take away at the end of the course. Your fact find is available to use throughout the course as a record of your goals and financial circumstances. You can download your fact find now so that you’re ready to use it later this week. Record your own details and, if you wish, those of your partner.

This fact find is different to the documents you complete when acquiring financial products like investments and mortgages. The fact find for Managing my money is intended to provide a full summary our personal financial circumstances. When acquiring specific financial products your financial adviser or financial product provider (e.g. your bank) will only require details about your financial circumstances that are relevant to the financial product you are intending to acquire.

You can also access a handy short glossary to the course.

A note about financial advice

This course provides the information, frameworks and financial planning guidance needed to manage your finances and to assist in making financial decisions.

However, course contents do not constitute ‘advice’ with regard to which specific financial products you should use or which financial services providers you should do business with. Consequently the course educators and facilitators cannot answer questions about matters relating to such financial advice.

If you need specific individual financial advice you should contact an authorised financial firm or financial adviser.

This course is presented with the kind support of True Potential LLP.

The True Potential Centre for the Public Understanding of Finance (True Potential PUFin) is a pioneering Centre of Excellence for research in the development of personal financial capabilities. The establishment and activities of True Potential PUFin have been made possible thanks to the generous support of True Potential LLP, which has committed to a five-year programme of financial support for the Centre totalling £1.4 million

1.1 The economic backdrop

Everyone – directly or indirectly – is affected by the good and bad events in the economy. One way or another, those of us in wealthy societies are all shoppers in the financial supermarkets. The video highlights some of the many issues that have had an impact on households and personal finances in recent years.

Transcript

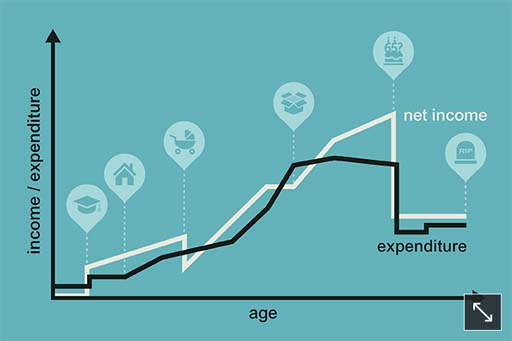

1.1.1 The life course

Considering the life course as a series of stages provides a means of thinking ahead and seeing an overall pattern.

Figure 1 illustrates a ‘typical’ pattern where youth, adolescence and young adulthood lead on to becoming part of a couple, where adulthood entails working and having dependent children who later on become independent themselves. The later part of the life course is usually marked by old age and retirement from working.

Of course, the life course won’t be the same for everyone; some people won’t form part of a couple or won’t have children, and some will experience family breakdown or bereavement.In relation to personal finance, the idea of the life course is helpful because it encourages planning ahead for the financial implications of each stage. For example, many people delay thinking about their provision for retirement because they don’t want to think about growing older, but they often come to regret this later in life when they realise that they would have benefited from earlier planning. Thinking in terms of stages in the life course might help to overcome this natural aversion. It provides a framework for thinking about possible life events such as marriage, parenthood, retirement, or even death, and this can make it easier to think ahead constructively.

No one can know exactly what will happen in the future. Financial capability – the ability to understand finances and make sound financial decisions – involves thinking ahead and planning for what might happen in the future; this includes not only things that we hope for, but also things that we hope will not happen.

Sensible planning takes into account the fact that the future may bring events that can be anticipated, as well as unexpected events with financial implications – unexpected bills or periods of illness or unemployment. Planning for the unexpected is one important aspect of financial capability.

1.1.2 The life course game

| Total income | £2500 |

| Mortgage and bills | £1150 |

| Cars and other travel | £130 |

| Cinema, takeaways, fun! | £70 |

| Emergency fund saving | £200 |

| Food and household goods | £500 |

| Holidays | £150 |

| Home contents insurance | £0 |

| Life insurance | £0 |

| Pension saving | £0 |

| Total spending | £2200 |

| Budget surplus/shortfall | £300 |

Try to work out what could happen to the Pennys’ financial position in the scenarios given below. Avoid overcomplicating your analysis – just ascertain whether these would be good or bad financial events for Mr and Mrs Penny, and how important they would be.

- Mrs Penny becomes permanently disabled.

- Mr Penny is made redundant.

- The Pennys’ car breaks down.

- The Pennys’ children move out of the family home after they finish college.

Now look at the Pennys’ spending. In terms of covering the cost of life’s events, are they taking any risks? You might want to draw up a revised budget for them.

1.1.3 Your life plan

Here’s the life course graph again. What do you think your own personal and financial circumstances might be in five years’ time?

If you had answered this question five years ago what would your expectations have been? How closely would your answer have matched what has actually happened to you?

Does this lead you to revise what you think your circumstances might be in another five years?

What factors are influencing your thinking about the outlook for your personal and financial circumstances?

1.1.4 Starting your financial plan

Your first step in exploring financial capability is to think in a systematic way about the goals you have in your life. The process is called financial planning. In order to plan effectively you need to take into account the end goal.

This is the first occasion on which we want you to make use of your personal financial plan and fact find (from now on, called simply the ‘fact find’). A fact find is a means of setting out your current financial position and linking it to your goals in life. It’s a summary of your financial health, and can be used when you’re in discussions with advisers about financial decisions that need to be made. Download this now if you haven’t done so already, and when you’ve identified your goals record them in the first two rows, under the heading ‘Assess’.

Try noting down your three most important goals.

Goals are affected by individual circumstances and backgrounds, and by the kind of society in which the person or household is living.

People don’t form goals in a social vacuum. Many goals in life are ‘self-interested’, while others relate to political, ethical or religious commitments. Some people have a goal of helping achieve social fairness; they might be altruistic with their money and give to charity, or they might buy Fairtrade products that don’t exploit individuals or communities. Developments in ethical banking reflect these changes. Similarly, increasing awareness of environmental issues has affected some people’s goals by changing their pattern of consumption, which might lead them, for example, to cut back on unnecessary travel.

It’s very likely that goals will change in the course of a life as events unfold – as people form or leave relationships, have children, experience illness or disability, learn to cope with bereavement, move in and out of different household or family groupings, or live and work in different countries.

Think about goals with financial implications that, say, a young, single adult might have:

- take a holiday abroad next year

- buy a flat within ten years

- help the homeless

- get married in three years’ time

- have a comfortable retirement.

These goals relate to different time periods. In financial terms, ‘short term’ is normally taken to be under five years, ‘medium term’ is around five to ten years, and ‘long term’ is normally more than ten years. Taking a holiday next year and getting married in three years’ time are short-term goals. Buying a flat within ten years is a medium-term goal. Providing for a comfortable retirement is a long-term goal. Helping the homeless is an ongoing goal.

1.1.5 Prioritising

Thinking about goals is one starting point for financial planning, but the achievement of those goals may be constrained by the resources that a household has, together with its commitments.

For most households, achieving their goals is subject to the financial constraint of the resources that are available. Some households have goals that are not as affected by the available resources. In these cases the resources are not functioning as a constraint on financial plans. This may be because the household is rich, or because it has goals that are not financially demanding. Other households have goals that are severely constrained by available resources. In these cases, money difficulties are a constant source of anxiety and severely inhibit goals. Here the main goal might be basic financial survival.

So, an important question is whether all the goals can be achieved, given the financial constraints. Whether a person is able simultaneously to take a holiday next year, help the homeless, get married and buy a flat depends on their financial constraints. If the person can’t afford to do all these things, then choices have to be made. There’s a trade-off between using money and resources in some ways rather than in others. A trade-off involves giving up something in order to have something else that is preferred: taking lavish holidays means not being able to buy a flat. Which is more important? It’s necessary to prioritise.

- Take another look at your list of three most important goals. Have you listed the goals in any particular order?

- Try listing the goals in order of priority for you, given your circumstances and resources.

- Are there trade-offs between your goals?

- Has this prompted you to rethink any of your goals?

When doing (or buying) something involves giving up something else, the real cost is what would have been done (or bought) instead. This is called the opportunity cost. For example, the opportunity cost of buying a car is what would have been done (or bought) instead. The money might be spent on other things, or it might be saved or given away; it might be used to reduce or pay off existing debt. The opportunity cost of buying the car is the best alternative that is forgone (done without) in order to buy the car, such as buying a holiday with the money instead.

Time, as well as money, is a scarce resource. Most of us can’t do all the things we want to partly because we don’t have the time. The opportunity cost of you spending your time studying this course is what you would have done with your time if you hadn’t been doing this. It’s the best alternative use of your time. (If you wouldn’t have done anything else, then you’re not giving up anything to study the course, and so the opportunity cost would be zero.) Some busy people are particularly ‘time-poor’, even though they may be rich in a monetary sense.

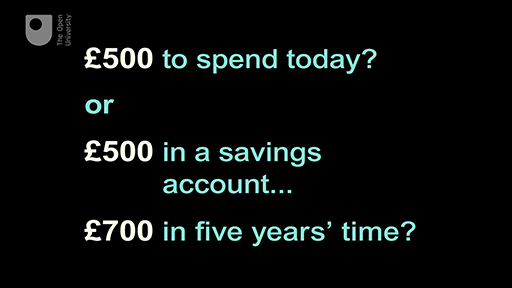

Sometimes trade-offs have to be made between doing something now and doing it in the future. If you spend money now, it’s not available for later. There’s a tendency for people to place a greater value on £100 to spend now than on £100 to spend in one or two years’ time. You’ll find there are good economic reasons for this – especially because of inflation, which you’ll look into in Week 2.

But there are also rewards for not spending now in order to have more to spend later. If you’re hoping to build up a target amount for a future purchase or a pension, then just a few years’ delay in starting to put the money aside can greatly increase theamountyou have to put aside to be sure of meeting the target.

In addition, many financial products involve trade-offs of their own. For instance, financial investment tends to involve a trade-off between risk and return: the higher the expected return, the higher the risk attached. Which is the right product depends not only on how much risk – if any – can be afforded, but also on how risk averse a person is. Risk-aversion is the preference for a lower, but more certain, return rather than a higher, but less certain, return, other things being equal.

1.2 Your personality can seriously affect your finances

Are you risk averse or a risk taker? Find out about the behaviours that can lead to poor financial decisions and start to build your financial planning model.

Have you ever thought about how far your personality and, in particular your approach to risk taking, affects your financial decision making?

In this video Mark Fenton-O’Creevy, Professor of Organisational Psychology at The Open University Business School and an expert in behavioural finance, introduces the way behavioural biases affect personal financial decisions.

Transcript

1.2.1 Betting the house

Most of us like to have a gamble once in a while – even if it’s just buying a lottery ticket or backing a horse in the Grand National. How big is your appetite for risk taking? How much are you prepared to lose on a bet – £5? £20? £100? Maybe even £1000? Ashley Revell was prepared to take on a huge gamble. Was it bravery or madness?

Transcript

Activity 1

Would you say you’re risk averse? Or are you a risk taker?

What factors or changes to your circumstances might affect your answer?

Go to the fact find and log your appetite for risk in relation to your three goals.

Discussion

The video on ‘betting the house’ depicts an extreme, high-risk and, in truth, reckless way of managing money and making financial decisions.

The reality with financial decisions is that there are many shades of risk taking between being completely risk-averse to being prepared to take on higher risks that can deliver higher returns. In fact some decisions that may seem risk-averse, like leaving savings in an instant access account offering a low, but guaranteed, return expose you to the risk that the balance of your savings may grow more slowly than the rate of price inflation, thereby reducing, over time, the value of goods your savings can buy.

We’ll learn more about how inflation impacts our personal finances in the second week of the course. Later we’ll look at the historical evidence about the correlation between risk taking and returns.

The picture you’ll get by the end of the course is that working out what risks are worth taking is more complex than, at one extreme, deciding to put your life’s savings on a single bet at a casino or, at the other extreme, just leaving your saved money in your bank account.

1.3 Building your financial planning model

Martin introduces you to the financial planning model – a process with which you’ll become very familiar as you progress through the course and develop your financial capability.

Transcript

Financial capability involves being able to work out a financial plan for achieving a goal, given the constraints that you face. Constraints include things like income and existing savings, personal circumstances such as having to care for children or elderly relatives, and emotional factors such as how you feel about taking risks. For example, if your goal is to reduce debt worries, then financial capability involves better debt management. If you decide to consolidate debts into one package and then pay them all off systematically, some of these packages cost less than others (other things being equal). If there are debt problems, it’s better to seek advice from professional bodies like the government’s Money Advice Service (MAS), or from Citizens Advice or StepChange, rather than going to a ‘loan shark’ who charges extremely high rates of interest. Alternatively, if you’re saving to buy a flat, some savings schemes offer a better return than others (other things being equal), and all of them are likely to be better than stuffing cash under the proverbial mattress.

Seeking out well-informed advice and choosing better products, given constraints and goals, would be evidence of greater financial capability.

1.3.1 Applying the financial planning model

To make sure that your financial decisions are well managed, you should start to apply the financial planning model to financial decision making.

Think of a recent financial decision that you’ve taken and analyse your own process of financial planning. Try to remember each stage of your decision and have a go at analysing the stages in terms of the financial planning model. The decision could be something to do with moving house, buying a car, changing jobs, borrowing money for a project.

You’ll apply the financial planning model to your own financial circumstances as you work through the course to help you build your financial plan and complete your fact find.

If you were to make a similar financial decision right now, would you approach it differently?

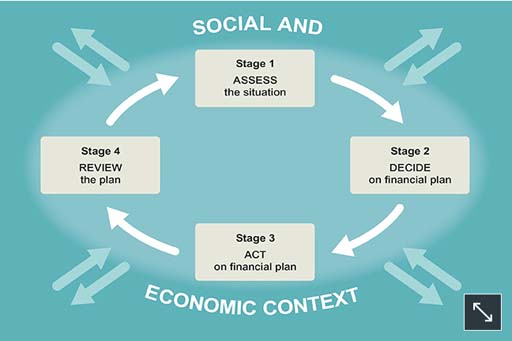

1.3.2 Goals – the social and economic context

So far you’ve seen that financial planning can be understood as a sequence of stages: assess, decide, act and review – a continuous process. But as you see in this developed version of the financial planning model, these four stages also need to be understood in a broader context, as shown by the arrows pointing into and out of the process.

Thinking about your own life, you’ll be aware that your financial goals, and the ways you go about trying to achieve them, can be influenced by social factors such as your values, culture or religion as well as by economic factors. In terms of religious values, for example, the taking or paying of interest is prohibited under sharia law, as it was by the Roman Catholic Church in earlier centuries. Approaches to charitable donations, the giving of care and financial support to family members are also affected by contextual social factors.

The planning process impacts not only on individuals but also on the wider society. In the financial planning model this is shown by the arrows pointing outwards. Take a couple of instances: if many people decide to buy a flat, there is likely to be a rise in the price of flats which will have knock-on effects; or if many people decide to reduce their indebtedness, spending will fall and high-street retailers will face falling profits.

These examples – of increases in property prices and falling retail sales – illustrate the cumulative effect of many individual decisions, and how far the impact of individual decisions can spread. The effects were not an intended consequence of the individuals’ decisions at the time, and they can be different from what people individually expect. For instance, if an individual person or household goes on a spending spree, the consequences mainly affect that individual; but if a significant proportion of households go on a spending spree, there will be cumulative effects which have an impact throughout the economy.

Sometimes the effects of many people doing the same thing can become a ‘bubble’, and this can impact much more widely: every bubble eventually bursts, and when it does it sends ripples throughout society. In the late 1980s a large number of people wanted to buy property. Prices rose steeply in 1988 and 1989, but the bubble burst and property prices fell sharply in the early 1990s. This had severe consequences for some of those who bought when prices were at their peak. In the late 1990s there was a stock market bubble, with many people buying shares, especially in companies related to new technology and the internet. But from 2000 to 2002 the value of many stocks and shares fell dramatically, with negative financial impacts for those holding such stocks and shares. Similarly, throughout the 2000s property prices again rose sharply before falling with the onset of the financial crisis in 2007. After 2009, however, property prices started to rise again as the UK economy recovered from the economic recession that followed the financial crisis.

As you see, what individuals and households do with their money is not separate from the larger economy; in fact, it helps to define that larger economy.

Now take another look at the goals you listed earlier in your fact find. Think about social and economic influences on these goals. If the influences had been different, would your goals have been different?

It can be hard to imagine having had different influences. But if any of your economic circumstances or your social and cultural background were different, it is likely that your goals would be too. As you work through the next few weeks of the course, take time to reflect on some specific examples.

1.4 Try the bad habits test

As you heard earlier from Mark Fenton-O’Creevy, there are good reasons why we sometimes make bad financial decisions, even if we’re pretty smart about most other things in life.

Find out if you’re suffering from some of the factors that make personal financial choices particularly difficult – perhaps we should call them the ‘perils of personal finance’.

Transcript

You’re almost at the end of the first week. When you’ve explored your bad habits, see what you’ve learned so far in the first test.

1.5 Week 1 quiz

This quiz allows you to test and apply your knowledge of the material in Week 1.

Complete the Week 1 quiz now.

Open the quiz in a new window or tab then come back here when you're done.

1.6 Week 1 round-up

In Week 1 you’ve seen:

- how to construct and use a financial planning model

- how our financial resources and needs alter over the life course.

Next week you’ll look at income as you meet one of the key financial challenges for all households – how to draw up and run a household budget.

You can now go to Week 2: Income, taxation and benefits

1.7 Further reading

If you want to know more about the work of the True Potential Centre for the Public Understanding of Finance (PUFin) and its mission to improve personal financial capability, check out the centre’s website. The centre, generously funded by True Potential LLP, has a mission to develop teaching and undertake research to help improve public financial capability.

References

Acknowledgements

This unit was written by Martin Upton and Jonquil Lowe

Except for third party materials and otherwise stated in the acknowledgements section, this content is made available under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 Licence.

The material acknowledged below is Proprietary and used under licence (not subject to Creative Commons Licence). Grateful acknowledgement is made to the following sources for permission to reproduce material in this unit:

Unit image

Figures

Figure 4 © iStockphoto.com/cherezoff

AV

The economic backdrop © The Open University (contains archive © BBC)

Your personality can seriously affect your finances © The Open University (contains © 123RF and Patrick Landmann/Science Photo Library)

Betting the house © The Open University (contains © BBC archive, 123RF images and REX/Ken McKay)

Every effort has been made to contact copyright owners. If any have been inadvertently overlooked, the publishers will be pleased to make the necessary arrangements at the first opportunity.

You can now go to Week 2: Income, taxation and benefits

Don't miss out:

1. Join over 200,000 students, currently studying with The Open University – http://www.open.ac.uk/ choose/ ou/ open-content

2. Enjoyed this? Find out more about this topic or browse all our free course materials on OpenLearn – http://www.open.edu/ openlearn/

3. Outside the UK? We have students in over a hundred countries studying online qualifications – http://www.openuniversity.edu/ – including an MBA at our triple accredited Business School.