Building number confidence: Budgeting

| Site: | OpenLearn Create |

| Course: | Building number confidence: Budgeting |

| Book: | Building number confidence: Budgeting |

| Printed by: | Guest user |

| Date: | Sunday, 26 July 2026, 2:40 AM |

1. Money and budgeting basics

Money

Money exists in numerous forms, including physically as coins and bank notes, and digitally in bank accounts and credit cards. It is used to pay for goods and services.

UK coins come in several values (1p, 2p, 5p, 10p, 20p, 50p, £1 and £2) and are designed in various sizes, shapes and colours to make it easier to tell them apart.

The Bank of England issues notes for larger values, each with a different colour and design: blue for £5, brown for £10, purple for £20, and red for £50.

These same principal colours are used in the design of notes from the three issuing banks in Scotland (Bank of Scotland, Clydesdale Bank and Royal Bank of Scotland).

Explore current designs via the following external webpages:

- The Royal Mint | Coin Designs and Specifications

- Bank of England | Current banknotes

- UK Finance | Committee of Commercial Banknote Issuers » Banknotes

Currency

The 'currency' of a country, or economic area, is the money system in use and its standard unit of value.

The UK's currency is Sterling - or 'Pound Sterling', after its main unit, the pound. The pound sign (£), or the international currency code GBP, denote values in Sterling.

The UK uses a decimal system for money. One pound is made up of 100 pence (p), so 50p is half of a pound, and 1p (one penny) is one hundredth of a pound.

This means pounds and pence work like whole numbers and decimals. For example, £1.50 means 1 pound and 50 pence.

Converting between pounds and pence

Pence into pounds: divide the number of pence by 100. For example, 125p is £1.25.

Pounds into pence: multiply the number of pounds by 100 (tip: move the decimal point 2 places to the right). For example, £3.75 is 375p.

Budgeting

Budgeting - keeping a track of your money, your income and expenditure, planning and making decisions about spending and saving - helps you to stay in control and meet your financial goals.

Budgeting involves using everyday numeracy skills and operations. For example:

- You use addition to add up your income from different sources or total your spending over a week or month.

- You use subtraction to work out how much money you have left after paying for bills and other expenses.

- Sometimes, you might need to use multiplication to plan for regular costs (like a weekly payment across a month), or division to split your money into savings or spending categories.

- You may also use rounding to estimate costs or check whether you have enough money to cover a purchase without needing to calculate the exact total.

Building confidence with these simple operations makes it easier to manage your money. If you need to work on these skills, check out our other course: Number Confidence for Everyday Life.

Budgeting check

Harry grows courgettes in his garden but always has more than he needs. He sells 13 courgettes to friends and family at 50p each, which he will donate to charity.

How much money will he be able to donate in pounds and pence?

To find out how much money Harry will donate, multiply the number of courgettes sold by the price of each courgette:

13 courgettes × 50p = 650p

Now, convert pence into pounds and pence. There are 100 pence in £1:

650 ÷ 100 = £6.50

Harry will be able to donate £6.50 to charity.

2. Understanding your payslip

Knowing exactly how much money you have coming in each month is the first step of the budgeting process. Keep a check on your payslips to ensure you have been paid the correct amount and that any deductions have been made at the correct rate.

Payslips come in various formats, however they all include these key components:

- Gross income (your salary, or basic pay)

- Additions (such as overtime and any allowances)

- Deductions (including tax, National Insurance and pension contributions)

- Net income (your take-home pay after deductions).

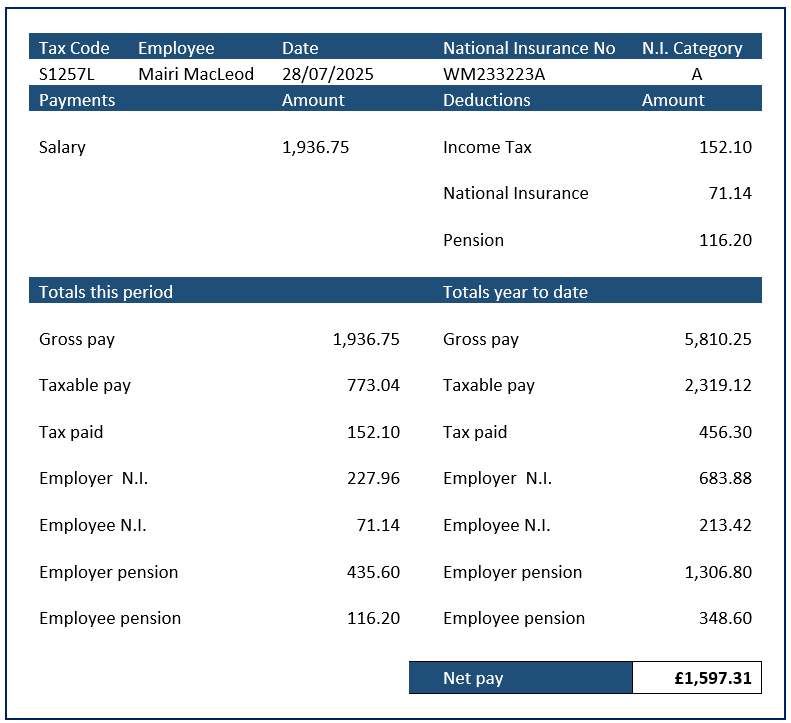

Let's have a look at Mairi's recent payslip.

Gross income

This is your salary, or your basic pay, before any additions and deductions). Mairi receives a monthly salary of £1,936.75. In this payslip Mairi's salary is listed under 'Payments'.

Gross pay can often be worked out by multiplying the number of hours worked by the hourly rate of pay.

For example: If someone works 10 hours at £20 per hour, their gross pay is 10 × £20 = £200.

Additions

These are anything added to your basic pay, such as overtime, on-call allowance or bonuses and would be listed under 'Payments'. Mairi has no additions to her basic pay this month.

Deductions

Deductions are anything taken off your basic pay. The most common are Income Tax, National Insurance and pension contributions (click headings below to expand).

Income Tax is tax paid to the Government, on your annual income. Not all types of income are taxable, and most people are entitled to a tax free allowance.

Your tax code is issued by HM Revenue and Customs (HMRC) and informs how much tax should be deducted by your employer on behalf of the Government.

Your Personal Allowance is the tax-free amount you can earn during a tax year (6 April to 5 April the following year). Any earnings above your personal allowance are taxed, at varying rates depending on income (there is no tax free allowance for those earning over £125,140).

Mairi's payslip shows that her tax code is S1257.

- S indicates that she pays tax in Scotland.

- 1257 indicates her (tax free) Personal Allowance (£12,570).

- L confirms she is entitled to the standard (tax free) Personal Allowance (currently £12,570).

Tax of £152.10 has been deducted.

Various factors can influence your tax code. Visit Tax codes: what your tax code means for an overview and further information.

In Scotland, (2025) tax rates start at 19% on earnings from £12,571 to £15,397, rising incrementally to a top rate of 48% on earnings over £125,140. Visit Income Tax in Scotland and Income Tax: introduction for current rates and further information.

National Insurance contributions qualify you for certain benefits and a State pension when you reach retirement age.

Your unique National Insurance number ensures your National Insurance contributions and tax are recorded against your name only.

Mairi's payslip shows that National Insurance of £71.14 has been deducted. Note that her employer is also required to contribute, on her behalf, at a higher rate.

Visit National Insurance: introduction for an overview and further information.

Workplace pension schemes provide an income when you retire. Pension contributions are deducted from your salary, and your employer may also contribute to this pot.

Mairi's has 6% of her salary deducted each month towards her workplace pension (£116.20 this month) and her employer also contributes at an enhanced rate (£435.60 this month).

UK employers are required to provide automatic enrolment to employees who meet certain criteria.

What is automatic enrolment? | Department for Work and Pensions (DWP), 0:40

Other possible deductions include student loan repayments, trade union subscriptions, cycle-to-work scheme loans and charitable donations.

Net income

This is your 'take-home' pay, what will be paid into your bank account, after any additions and deductions have been made. Mairi take-home pay this month is £1,597.31.

Budgeting check

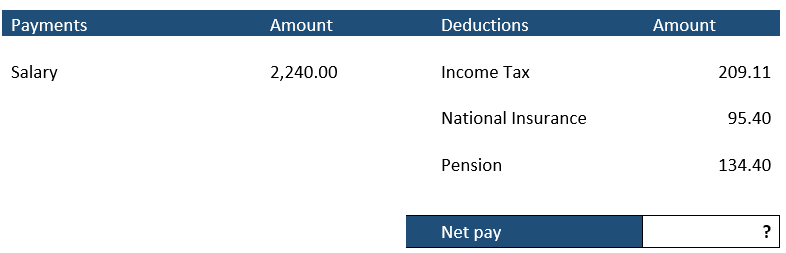

Murdo's payslip shows a gross pay this month of £2,240.00 and the following deductions:

- Income Tax: £209.11

- National Insurance: £95.40

- Pension Contribution: £134.40

What is Murdo's net (take home) pay?

£1.801.09

£2,240.00 (gross) - £438.91 (total deductions) = £1.801.09 (net).

3. Personal and family budgeting

A budget is a plan for your money.

Budgeting helps you stay in control of your finances, avoid unnecessary debt, make the most of surplus, and reach your financial goals.

Perhaps you want to:

- simply ensure your income covers your expenditure;

- save for a holiday or major purchase;

- put money aside for a rainy day.

Creating a budget makes it much easier to see the full picture of:

- the money you have coming in every month;

- how much of this goes to essential spending (such as rent/mortgage, electricity, food etc) and how much is available to cover other expenditure;

- where savings can be made, for example by shopping around for better deals, or cancelling subscriptions.

4. Budgeting steps

Step 1: Calculate your total monthly income

The first step is to ascertain how much money you have coming in, each month, including:

- your take-home pay (after tax and other deductions);

- benefits you receive, e.g. child benefit;

- any other income e.g. child support.

List these, on paper or in a spreadsheet, and add them together (a spreadsheet or budgeting app will do this for you) to find your total monthly income.

Step 2: Calculate your total monthly outgoings

Using bank statements and other financial documents (bills, credit agreements etc), list all your outgoings, both fixed and variable, separating essential, from non-essential (or 'nice to have') spending.

Fixed

These are regular monthly payments (see examples below) often set to leave your bank account via direct debit or standing order.

- Essential: rent/mortgage, gas/electricity, broadband, phone contract, insurance.

- Non-essential: gym membership, streaming services and subscriptions.

- Debts: car finance, loan repayments, credit cards, bank charges.

- Savings: regular payments to savings account or private pension.

Divide any annual payments by 12 to work out a monthly cost.

List these in a new column - under a heading 'Outgoings' - in the budget document you started in step 1.

Variable

These are payments, using cash or debit card for example, which may vary from month to month. Calculate your average monthly spend on each.

- Essential: food, car/transport costs (fuel, servicing, repairs, MOT, bus/rain fares), childcare, toiletries, ’pay as you’ mobile, dentist, optician.

- Non-essential: entertainment, eating out, days out, hobbies, impulse spending.

- Other: birthdays, Christmas, holidays.

Add these to your list of outgoings - again dividing any annual payments by 12 to work out a monthly cost - and sum them to find your total monthly outgoings.

Step 3: Compare your total income with total outgoings

Subtract your total monthly outgoings from your total monthly income. Does your income cover your total outgoings?

You may find that your monthly expenditure exceeds your current income. Can you increase the money you have coming in and/or reduce costs, for example by shopping around for better deals, or cancelling subscriptions?

If you break even, or have a surplus, reducing costs could enable you to put money aside for contingencies (emergency repairs for example), towards planned purchases or into savings.

Budgeting check

Mairi has created a monthly budget plan using a spreadsheet app.

Starting with the balance left in her bank from last month, she has set up the spreadsheet to automatically subtract each item of expenditure and update the balance.

Mairi has allocated £370 this month for weekly shopping and miscellaneous spending. Will she be able to do the same again next month if all other income and expenditure stay the same?

| Description | In | Out | Balance |

|---|---|---|---|

| Carried forward | 37.50 | ||

| Salary | 1475.00 | 1,512.50 | |

| Mortgage | 750.00 | 762.50 | |

| Council tax | 114.00 | 648.50 | |

| Broadband | 35.00 | 613.50 | |

| Phone | 24.00 | 589.50 | |

| Gas/electric | 90.00 | 499.50 | |

| TV | 13.00 | 486.50 | |

| Gym | 47.00 | 439.00 | |

| Bus to work | 64.00 | 375.50 | |

| Weekly shop & misc spending | 370.00 | 5.50 |

After paying all her fixed expenses, and setting aside £370 for shopping and miscellaneous spending, Mairi has a balance of £5.50 in her account.

Starting a new month with the £5.50 carried over, the costs she has budgeted for would result in a minus balance (-£26.50) .

| Description | In | Out | Balance |

|---|---|---|---|

| Carried forward | 5.50 | ||

| Salary | 1475.00 | 1,480.50 | |

| Mortgage | 750.00 | 730.50 0 | |

| Council tax | 114.00 | 616.50 | |

| Broadband | 35.00 | 581.50 | |

| Phone | 24.00 | 557.50 | |

| Gas/electric | 90.00 | 467.50 | |

| TV | 13.00 | 454.50 | |

| Gym | 47.00 | 407.50 | |

| Bus to work | 64.00 | 343.50 | |

| Weekly shop & misc spending | 370.00 | -26.50 |

Having the figures in front of you, particularly using a spreadsheet or app which updates the balance after each item, makes it easy to see where things are going wrong and adjustments have to be made.

We will have a look on the next page at how Mairi used her £370 allowance this month, but she may have to reduce this. It may also be possible to reduce some of her fixed expenses, for example by shopping around for better deals.

5. Planning your budget

Knowing exactly how much money you have coming in, and how much you have going out, will help you to achieve, your financial goals.

- Decide what you want to achieve, and build this into your plan. For example, if you are saving for a holiday, or major purchase, work out how much you will need to set aside each month and list this under your outgoings. You might also consider setting up a standing order to move this amount into a savings account each month.

- Aim to put a regular amount aside, however small, to create a buffer which will help to cover unexpected costs.

- Monitor your budget regularly, at least monthly. This will help you to adjust your plan in good time, for example you may find that a direct debit has increased.

- Monitor your personal spending to ensure you do not exceed the amount put aside for this in your budget plan.

Setting clear, realistic goals, and monitoring progress, will help you to stick to your budget.

Calculating savings goals

You can calculate savings goals using common operations, like multiplication and division. Click headings below to expand.

Subtract the total of all your expenses from your total income.

For example, if your net pay is £1500 and your total expenses are £1000:

£1500 - £1000 = £500

You have a surplus of £500 which you could deposit into savings.

Multiply the amount you plan to save each month by the number of months.

For example, if you save £60 per month for 6 months:

£60 × 6 = £360

In 6 months you will have saved a total of £360.

Divide the total amount you want to save by the number of months.

For example, if you want to save £1000 in 5 months:

£1000 ÷ 5 = £200

You need to save £200 each month, for 5 months, to reach your goal of £1000.

Safe savings options

The safest place to save money and earn a predictable amount of interest is a regulated bank or building society savings account protected by the Financial Services Compensation Scheme (FSCS). There are other options, but they can be risky. For example, the value of Stocks and Shares can rise or fall, and you may get back less than you invested. Cryptocurrencies are also highly volatile and not regulated in the same way as traditional financial products.

It's a good idea to get independent financial advice before investing, especially if you're unsure about the risks or which options suit your needs.

Using a cashbook

A Cashbook is a record of your spending over a specific period which allows you to check that you are within budget and how much cash you have available at any given time.

Mairi's budget allows £370 a month for weekly shopping and miscellaneous spending, and using a spreadsheet app, she has kept a note of everything she has spent this month.

| Date | Description | Cost (£) | Balance (£) |

|---|---|---|---|

| 01.06.25 | Allowance | 370.00 | |

| 04.06.25 | Weekly shop | 48.00 | 322.00 |

| 05.06.25 | New jeans | 39.00 | 283.00 |

| 11.06.25 | Weekly shop | 46.00 | 237.00 |

| 12.06.25 | Train travel | 21.60 | 215.40 |

| 18.06.25 | Weekly shop | 52.00 | 163.40 |

| 18.06.25 | Cash | 20.00 | 143.40 |

| 19.06.25 | Lunch out | 17.50 | 125.90 |

| 20.06.25 | Cinema trip | 16.00 | 109.90 |

| 24.06.25 | New bag | 28.50 | 81.40 |

| 25.06.25 | Weekly shop | 53.00 | 28.40 |

On 25 June, Mairi is still within budget with £28.40 remaining of the allowance she has set aside for shopping and incidental spending this month. If she left this in her account, she would still be in credit (just) - see the activity in the previous page.

Banking advice and apps

Your bank will provide budgeting advice and will likely provide an app to help you achieve your goals.

Banking apps will often allow you to put money into separate 'pots', and set up spending targets. Notifications can be sent to your phone to alert you to pending payments or when your card is used.

Other budgeting apps can help you manage your budget and savings across different bank accounts.

Getting help

If you find you are struggling to make ends meet, or with debt, Citizens Advice, StepChange and National Debtline provide free advice and support.

6. Comparing and selecting the best deals

To save money, and remain within your budget, make sure to compare similar deals for goods and services before deciding which to purchase.

The main consideration, of course, is likely to be the price, however there may be other considerations which make one offer more attractive than another.

Comparison tables

TA useful tool for comparing financial options is a comparison table. This typically lists the provider, products or services in the first column, with features and characteristics detailed across the rows.

Here is an example comparing sim cards:

| Provider | 5G Data | Mins/texts | Contract | Monthly cost |

|---|---|---|---|---|

| Purple Phone | 5GB | Unlimited | 1 month | £4.50/mth |

| MagiCall | 10GB | Unlimited | 6 months | £4.80/mth |

| iBlether | 50GB | Unlimited | 12 months | £4.99/mth |

Let's look at some examples of products and services you might want to compare.

Shopping

It's possible to save quite a bit on your supermarket shop by taking advantage of bulk-buying, special offers and choosing the store's own brands rather than named brands. Signing up for a store loyalty card, where available, can also provide extra savings.

For other purchases, shopping around or using price comparison websites can help you to find the best deal.

Budgeting check

Mairi always buys named brands for the following items, but how much could she save if she bought the store's own brands?

| Product | Purchased monthly | Name brand (£) | Store brand (£) |

|---|---|---|---|

| Baked beans | 8 | 1.40 | 0.42 |

| Cornflakes | 4 | 2.19 | 0.88 |

| Crisps (6 pack) | 4 | 2.15 | 1.00 |

Let's first compare the total cost of each item, for both the name brand and the store brand.

| Product | Name brand | Store brand |

|---|---|---|

| Baked beans | 8 x 1.40 = £11.20 | 8 x 0.42 = £3.36 |

| Cornflakes | 4 x 2.19 = £8.76 | 4 x 0.88 = £3.52 |

| Crisps (6 pack) | 4 x 2.15 = £8.60 | 4 x 1.00 = £4.00 |

| Total cost | £28.56 | £10.88 |

As you can see there's quite a difference in the total monthly cost of each. Changing brand for just these 3 products could save Mairi £17.68 on her monthly shopping bill.

Savings accounts

Savings accounts are types of bank, or building society, accounts which pay you interest on the money you have invested with them. This is usually a percentage of how much money you have in your account over a full calendar year.

The higher the percentage rate, the more interest you can expect to earn on your savings. However standard interest rates are variable, meaning they can rise or fall, depending on the base rate set by the Bank of England.

Some accounts offer a fixed rate, or a higher interest rate if you agree to certain conditions. For example, you may be required to pay in a minimum sum each month, or be restricted on how much you can withdraw. You might have to agree not to withdraw any money at all from your account for a fixed period of time. These types of accounts can help you save regularly towards a specific goal, such as a large purchase, however, you may be charged penalty fees if you are unable to meet the restrictions.

An 'instant access' account, with a lower interest rate, may be the better option, if you are creating a contingency fund, for example, and need to know that you can access your money at any time.

AER

The AER (Annual Equivalent Rate) enables comparison of savings accounts by indicating the percentage of interest you will receive each year, taking into account compound interest (interest paid on interest already accumulated).

For example,

Year 1: You deposit £2000 into a savings account offering 2.5% AER, and leave it untouched for a year.

Opening balance: £2000

Interest earned: £50

Balance including interest earned: £2050

Year 2: You decide to leave your money in the same account for another year, at the same rate. You are rewarded with interest on both your initial £2000 deposit, plus the £50 interest you received in year 1.

Opening balance: £2050

Interest earned: £51.25

Balance including interest earned: £2151.25

Note: AER does not take into account any fees you may be charged for accessing or managing your savings.

What is APR and how does it differ from AER?

APR stands for Annual Percentage Rate. It shows the total cost of borrowing money over a year, including interest and certain fees. You’ll see it used for things like loans, credit cards, and mortgages. APR helps you compare the overall cost of different borrowing options.

So, in short:

APR is used for borrowing – it shows the cost of a loan or credit.

AER is used for saving – it shows the return you’ll earn on savings.

More information about different rates, including Representative APR and Personal APR, can be found in the Glossary.

Budgeting check

Compare the following savings accounts. Which one offers the best deal for depositing £5000, and leaving it for 1 year with no withdrawals?

| Account name | AER | Fees |

|---|---|---|

| Bluebell Savings | 2.6% | £5.00 admin charge to open account and £12.50 annual charge |

| Heather Savings | 2.3% | No charges in year 1, £9 per annum thereafter |

Let's compare the balance in each account at the end of a year.

Bluebell Savings: Interest earned £130 (less £5 to open account and £12.50 annual charge) = £5,112.50

Heather Savings: Interest earned £115 (no charges in year 1) = £5,115.00

Heather Savings, with no fees for the first year, and no admin charge for opening the account, has come out on top with £2.50 more than Bluebell Savings over the same (first year) period of the account.

Note: Although Heather Savings offers a smaller annual charge, Bluebell Savings' higher interest rate is likely to make this the more profitable account in subsequent years.

Insurance

An insurance policy protects you financially by covering costs after events like illness, theft, or accidents.

Always shop around for the best deal for your car or home insurance, and when you receive an annual renewal quote, check that your current provider is still offering the best deal.

Think about how much voluntary excess (the money you agree to pay towards any claim you might need to make) is manageable. You might get a cheaper rate by agreeing to pay, for example, the first £500 of any damage to your car, but would you easily be able to do so?

7. Currency exchange for travel

Currency is the standard unit of value in the money system used within an economic area. For example, the Pound (or Pound Sterling) is the currency used in the UK, and in many European countries it is the Euro. The exchange rate is the value at which one currency can traded for another.

When travelling abroad, you will need to use the local currency in whatever countries you visit, and can exchange UK money for this before you go, at the airport, or when you arrive. Shop around for the best deals though - airport currency exchange kiosks, although convenient, often offer less favourable exchange rates or fees.

To change British money to foreign money - multiply by the exchange rate.

Foreign currency = British currency x Exchange rate

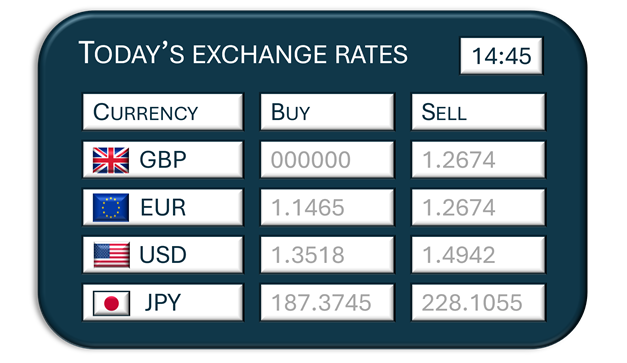

An exchange rate board shows how much of one currency you get when you exchange it for another.

You’ll usually see two columns: Buy and Sell.

Buy – This is the rate the currency provider offers when they buy foreign currency from you. For example, if you have US dollars and want to exchange them for pounds, this is the rate you’ll get.

Sell – This is the rate they use when they sell foreign currency to you. For example, if you want to buy euros for your holiday, this is the rate you’ll pay.

To calculate how much you will receive in exchange for your UK pounds (GBP), multiply what you wish to exchange by the 'buy' rate offered by the exchange service.

For example, if the current exchange rate for US Dollars is 1.3518, this means that for every pound (£) you exchange, you will receive 1.3518 dollars ($).

So for £500 you would receive $675.90 (500 x 1.3518).

Note that you may also need to pay currency conversion fees, which are charges for exchanging one currency into another.

Budgeting check

Before you head off on holiday, you wish to buy some Euros.

An exchange rate of £1 = €1.1465 is being offered by Simple Travel Money.

How much will you receive if you exchange £300 for Euros.

£343.95

300 x 1.1465 = 343.95

Converting prices when shopping abroad

You may also want to convert the price of items you are considering buying back into pounds, to help you decide if they are value for money.

To do this, divide the price of the item (in its foreign currency) by the exchange rate.

For example, if you want to buy a pair of shoes costing €150 and the exchange rate is £1 = €1.25.

€150 ÷ 1.25 = £120

So the cost of the shoes in pounds is £120.