2 The UK’s savings problem

The video in the previous section talked about the various reasons for saving money.

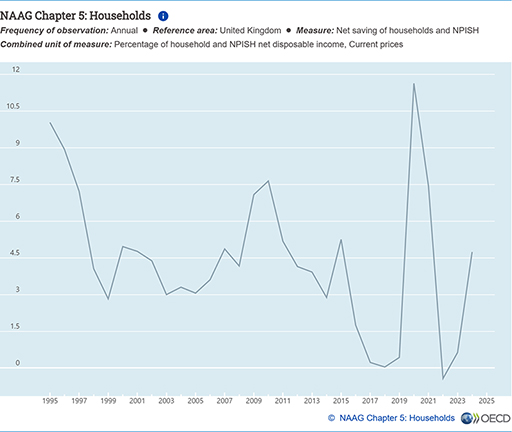

Whatever your own reasons for saving money, the reality is that the UK is not very good at doing it! The data in the tables below make this very clear. Figure 2 below shows net household savings rate, defined as “the portion of household income that is not spent on final consumption” for several OECD countries. It is evident that the UK has a lower savings rate than most other OECD countries.

Figure 2 shows the savings rate in the UK for the period 1995-2024. The figure suggests that the household savings rate has decreased over time. It increased briefly right after the Covid-19 lockdown. But then became negative in the year 2022.

Activity 2 Explaining the UK’s poor savings rate

Keeping Figures 1 and 2 in mind, what do you think are possible reasons for relatively low household savings in the UK?

Answer

There are several likely reasons for the low savings ratio in the UK.

The past decade has seen the value of real income – that is, income after adjusting for price inflation – fall for many people. With less money spare after meeting household bills, savings perhaps inevitably suffer.

Another reason may be the availability of debt. Borrowing money rather than drawing on savings is what many do to cover for life’s emergency spending or, say, the cost of a holiday. Yet this can be a very expensive way of covering such costs.

One reason for the decline in the UK’s savings ratio is that interest rates in the UK have been at historically low levels since the financial crisis in the late 2000s – and reached a record low in 2020 after the Covid-19 pandemic hit the UK. With the interest paid on savings accounts being so low, the incentive to save is less, and many may simply have opted to spend the money instead.

The Covid-19 pandemic did result in an increase in the savings ratio as a result of the reduction in the range of activities people could spend money on (like holidays). As life has slowly returned to normal in 2021 and 2022 the savings ratio has fallen back. The extreme pressure on household budgets caused by the recent surge in energy and other costs is likely to put more downward pressure on the ratio.