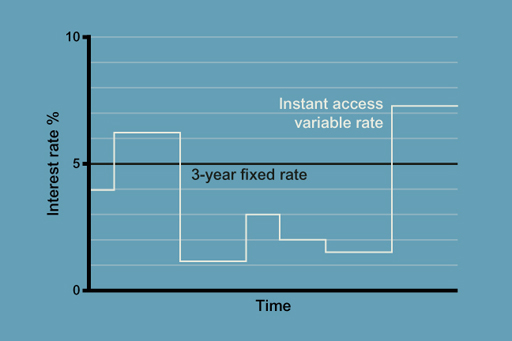

2.1 Variable rate and fixed rate savings products

Begin by listening to the audio, in which a young professional, Ryan, asks for help from personal finance expert Jonquil Lowe in finding his way through the many savings products on offer.

You join their conversation as Ryan asks about a savings product he’s come across called a ‘term bond’. The other savings options that are described are trackers, variable rate accounts and notice accounts.

Transcript

You looked at the impact of price inflation on investment earnings in Week 1, when you examined real interest rates. Index linked accounts are attractive to investors who want to guarantee that their savings are inflation-proofed.

In the UK, only National Savings and Investments (NS&I) periodically offers an inflation-proofed savings product in the form of index-linked certificates. These certificates are, however, only available to current holders of such investments and not to new savers. Existing savers - some 500,000 - can renew their investments when their existing certificates reach their maturity by buying new NS&I index-linked certificates for terms usually of up to 5 years. The returns on these index-linked certificates are now linked to the Consumer Prices Index (CPI) inflation rate.

At times of low inflation, the return on index-linked investments can seem unattractive, but they come into their own in periods when inflation is expected to be high. Most savings products do not offer inflation-proofed returns.