4.1.1 Age and lifestyling

There is a relationship between the age of an investor and the rational composition (or allocation) of investments. This factor relates to the investment principle of ‘lifestyling’.

Let’s look more closely at these influences on investment behaviour.

Age and asset allocation

An important factor when making decisions about the asset allocation is someone’s age.

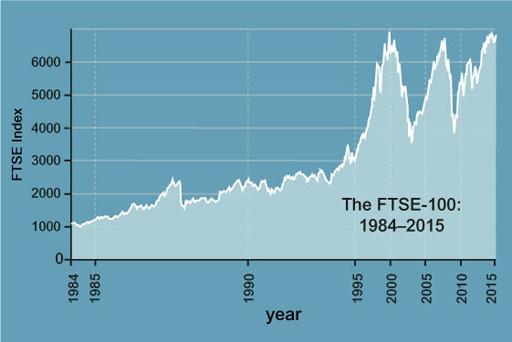

Investing solely in equities is more suited to long-term investment. If someone is retiring in a few years’ time, then investing solely in equities may be very risky. Looking at the graph in Figure 1 of the movement in the level of the FTSE 100, imagine what would have happened to the value of their investments if they were only holding shares and they retired in 2002/03 or 2008/09 – they would have seen the value of their fund severely hit. If, on the other hand, someone is 25, with 30 years or more to save, they can afford to invest more in equities. If not saving directly, but through a company pension fund, the pension fund managers will look at the age distribution of the members of the scheme when deciding on the asset allocation.

So, the asset allocation decision that may be appropriate when someone is relatively young may not be appropriate when close to retirement. This suggests that the pre-retirement years shouldn’t be entered into with too much risk. Indeed, asset allocation should be regularly revised and reviewed over the life-course.

Lifestyling

This kind of investment strategy takes age into account. It will automatically point an investor towards equities if they are under 30, and the cash/bond/equity mix will gradually be changed as someone gets older to put them into lower risk investments as they approach retirement.

Imagine if someone had 100% equities as they approached retirement. If the market did well, they might retire in splendour; if the market did badly, they might retire with little. In order to reduce this risk, an investor gradually sells equities and buys bonds over time, so that by the time the investor retires, their savings and investments are fully in cash and bonds and no longer bear stock market risk.