4 Alternative interest rate bases

Interest rates can be set in a number of ways.

- A variable rate, which can move upwards or downwards during the life of the loan. In the UK variable rates usually move in tandem with movements in the official rate of interest. Some products (called ‘trackers’) are specifically linked to specific rates of interest such as the official Bank of England rate.

- A variable rate with a ‘floor’. This is the same as a variable rate except that the rate cannot fall below a defined minimum level, known as the ‘floor’.

- A fixed rate where the rate is determined at the start of the loan and remains unaltered throughout the fixed-rate term. The rate will be based on what the lender has to pay for fixed-rate funds of the same term.

- A capped rate where the rate cannot rise above a defined maximum (the ‘cap’), but below this ‘cap’ it can move in tandem with movements of official interest rates. A variation to a capped-rate loan is a ‘collared’-rate loan where rates can move in line with official rates but cannot go either above a defined maximum (the ‘cap’) or below a defined minimum (the ‘floor’). Such products usually require the payment of a fee to the lender at the start of the loan.

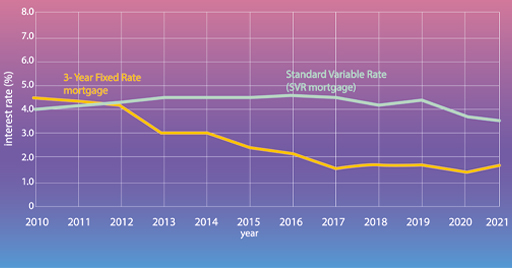

Most commonly, personal loans are set at a fixed rate; credit card debt and overdrafts are set at a variable rate; while mortgage lending is split between the four interest rate forms defined above.

Households with variable-rate mortgages are, along with most of those with credit cards and overdrafts, at risk from increases in interest rates. As mortgages account for a large proportion of personal debt, it is easy to see why the UK economy can be easily affected by even relatively small movements in interest rates.

Activity 2 Why are fixed-rate products popular?

Can you work out why debt products with fixed rates of interest are always popular with households regardless of expected future trends in interest rates in the economy? See if you can come up with your own answer to this before you look at the feedback.

Feedback

They are popular as they give certainty about the cost of borrowing. This makes things easier when it comes to running a household budget. With variable-rate products where borrowing costs could rise or fall it’s not straightforward to work out your budget.