8 Budget shortfall? Do not borrow!

When you consider your budgetary position it’s critical that you check whether the overall position is ringing any financial alarm bells. If you’ve taken on debt, for example, because of a continued excess level of expenditure over net income then your alarm should be ringing. This is a situation that could be caused by a number of factors.

To explore these circumstances, in this section you’ll use the example scenario of the Syme family, a household consisting of a lone parent and two children. The Syme household allows you to see how flows of expenditure and income relate to debt.

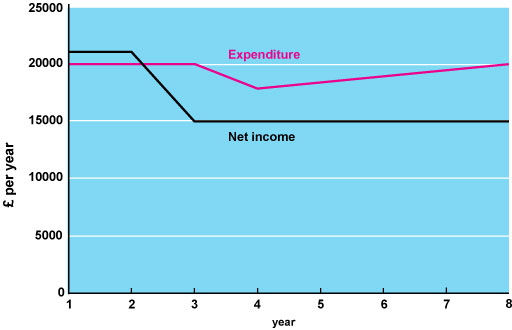

The main income earner in the household loses her full-time job in Year 2, and so household income falls below expenditure. This is a realistic scenario as research over many years shows that job loss is a major reason for households both getting into debt and having problems with debt (Citizens Advice, 2003; AOL, 2017).

From Year 3 onwards net income, made up of state benefits and earnings from part-time work, totals £15,000 per year. Expenditure remains constant at £20,000 in Year 3, and then the household manages to cut expenditure down to £18,000 in Year 4.

However, the shortfall between expenditure and income must be covered. This can be done by either using up any savings, or taking on debt, or a mixture of the two.

For simplicity, in this example assume that the Symes have no savings and that they borrow money to finance the expenditure over and above net income. This debt leads to expenditure increasing from Year 5 onwards as interest and other charges are added to existing household expenditure. This, in turn, will require more debt.

Such a situation is not sustainable in the long term and, eventually, the Symes will either have to make other cuts in expenditure or find a way to increase income. However, by forecasting how their finances will change in the coming years the Symes have given themselves time to take carefully considered action to address the situation. Such forward planning reduces the risk of having to resort to panic measured to resolve a financial problem.

Debt problems often arise when a household already has debt but then faces unexpected life events like those mentioned above. The Syme scenario highlights how certain life events, such as job loss, relationship breakdown or illness might lead to households having to take on debt. Other more predictable life events, such as full-time study, are easier to build into financial plans. A household, for instance, with one member who intends to go to university, might plan to finance current levels of expenditure through taking on debts and then using the benefit of increased earnings after graduation.

So one reason why individuals and households take on debt is to finance expenditure that is above income. Another reason is to spread the cost of expensive purchases, such as a car or house, over a number of years. In these cases, a household takes out a relatively large debt that is repaid over time. Taking out a debt to pay for these expensive items does not mean that the debt can be considered to be part of income. It might sometimes seem as though money that is borrowed can be used like income to pay for items. But the reality is, of course, that unlike income, debt is a liability that has to be repaid.

So effective financial management means incorporating your debt repayment obligations into your budget.