2 Good debt vs bad debt

Debt isn’t bad, but bad debt is bad. Borrowing money to have something now, that you’d otherwise need to wait for, isn’t automatically wrong.

However, to ensure that debt does not have a negative effect on your financial wellbeing, you should:

- prepare a careful budget that incorporates your debt planning,

- assess that you can comfortably afford debthe repayments, and

- select the cheapest possible loan available to you.

Having gone through all that, provided it’s a rational, controlled, planned decision, it is a question of personal choice. Real problem debts tend to stem from three main things:

- unexpected changes of circumstance

- habitual overspending

- ignorance – people who borrow without understanding the true impact of it, and the fact that if you owe money you have to repay it.

Activity 2 Case studies on debt

Here are four case studies of debt, some of which Martin Lewis referred to in the introductory video for this session. Some are good debts (sensible borrowing) and some are bad debts (ill-advised borrowing). Work out which category each case study falls into, and why. As you’ll see, it’s not always straightforward.

Answer

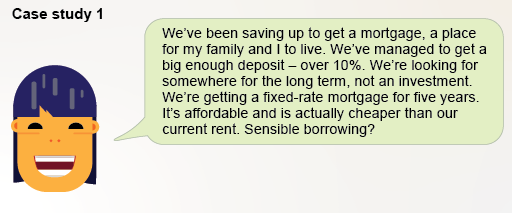

Case study 1: This is clearly sensible borrowing. The cost of borrowing is less than renting and the couple are paying an affordable mortgage to enable them to buy their own home. So it’s a good debt.

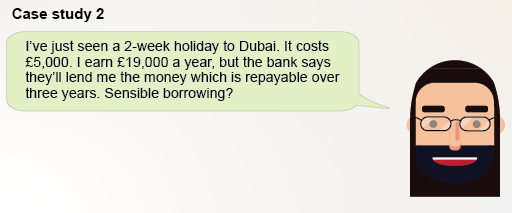

Case study 2: This is ill-considered borrowing. The loan is for a holiday costing more than a quarter of gross income. Repaying the loan will take three years for a holiday lasting a fortnight. How is next year’s holiday going to be funded? So this is a bad debt.

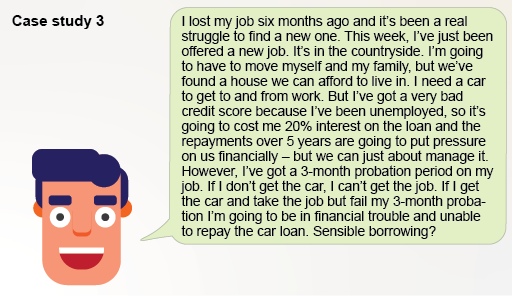

Case study 3: A trickier one – but arguably this is sensible borrowing. Most people get through the probation period when starting a job, so borrowing money to buy the car to get the job is rational behaviour. If repayments are made when due, there is likely to be an improvement in the borrower’s credit score, making future borrowing cheaper. If things go wrong, the car could be sold to help repay the outstanding loan. Overall though, we could call this a ‘grey’ debt.

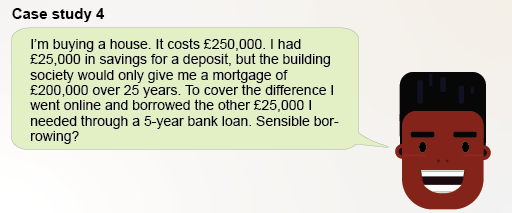

Case study 4: Not sensible at all. It is self-defeating. The building society will want to know how the ‘other £25,000’ is being covered. When they find that it is borrowed money, they will feed the cost of this to the borrower into their assessment of the size of the mortgage they are prepared to advance – with the likely outcome being that they will lend less than the original offer of £200,000. So clearly it is a bad debt.

So, whether borrowing is sensible depends on the circumstances. Certainly borrowing is not always a ‘bad thing’. In most cases it provides the means to buy key assets like property and cars. And in most cases borrowers are able to repay their debts without financial stress to themselves or their families.

You now need to turn to the factors that will affect your ability to borrow money and the terms on which money will be lent to you.

This brings you to the credit reference agencies and their scoring of your credit worthiness.