2 Understanding income tax

Employees

This section provides a basic introduction to income tax. Please note that the aim of the section is not to explain all aspects of income tax. For details of income tax relevant to your circumstances, please consult HM Revenue and Customs (HMRC [Tip: hold Ctrl and click a link to open it in a new tab. (Hide tip)] ).

Self-employed

If you are self-employed your earnings are not automatically taxed. Payments for the work you undertake are made without tax deductions. So the onus is on you to set aside the money that you will have to pay after you have made your annual tax return.

One way to help ensure you retain the money that is due to be paid in tax is to open a new bank account and place into it one-third of all the money you receive for your work. Having this separate account will help ensure that you do not spend the money before you have to pay it to the taxman. Setting aside one-third of your earnings is not a precise estimate of your tax bill but it is a good enough approximation that will avoid you getting into a panic when the tax is due. You may find the HMRC’s mobile app useful to learn more about paying taxes.

If you employ an accountant then they will help you with your tax planning.

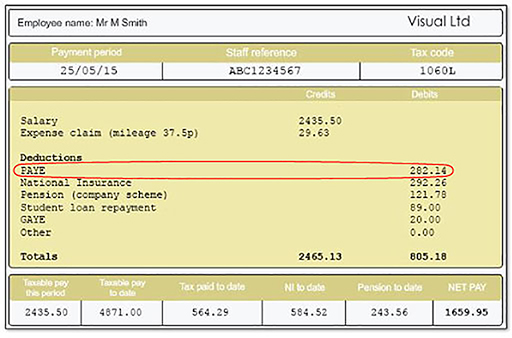

Deductions from your gross earnings

In the UK the top two payments that come out of your gross income are income tax and National Insurance Contributions (NICs), which are covered in the next section. Other deductions may be made too, like contributions to a pension scheme – but here you’ll focus on what for most people are these main two payments.

Income tax is imposed – levied – on almost all types of income including pensions (but it’s not payable on gifts, lottery winnings, Premium Bond winnings and ISA earnings). When it’s collected by HMRC through an employer (when the worker is employed rather than self-employed) it’s often referred to as a ‘pay as you earn’ (PAYE) tax.

Income tax is paid on income that is received by you within a given tax year (6 April in one year to 5 April of the following year).

You are allowed to earn up to a certain amount of money before having to pay income tax. This is called receiving the ‘personal allowance’ (PA), which is £12,570.

Historically, the PA increased with inflation. This meant that if your salary increased along with the prices of goods and services in the economy, then your personal allowance would increase as well. However, the PA has not increased in cash terms since 2021.

Moreover, the PA is frozen (i.e. it is unlikely to change) until 2031. The important thing to note is that due to frozen PA, you may pay more in income tax even though there may not be any increase in your real income (i.e. income after taking into account the impact of inflation).

You may like to try the following tax calculator on the BBC’s webpage to understand the impact of frozen thresholds on the tax that you are likely to pay.

The allowance is higher for certain groups of people, such as those who are registered blind. The plan had been for this personal allowance to increase each year in line with the rate of price inflation measured by the Consumer Price Index (CPI).

The personal allowance has an income limit of £100,000. If you earn above this limit the allowance tapers away, and those earning more than £125,140 a year don’t get any personal allowance.

Income tax in England, Wales and Northern Ireland

If you earn more than your personal allowance in any tax year, you will need to pay on the amount you earn above it. In England, Wales and Northern Ireland, there are three different tax bands as follows:

- income of £12,570 is tax free (recall personal allowance)

- income between £12,571 and £50,270 is taxed at 20% rate (i.e. basic rate)

- income between £50,271 and £125,140 is taxed at 40% (i.e. higher rate)

- income over £125,140 is taxed at 45% rate (i.e. additional rate)

Wales and Northern Ireland currently have the same income tax rates and bands as England. Partial powers to set income tax have been devolved to Wales although, to date, the effective tax bands and rates have remained the same as those in England.

For more details of these income thresholds, see the following link by the UK government: Income Tax Rates and Personal Allowances.

Income tax in Scotland

Since 1999 Scotland has had some discretion in respect of taxes and now has an increasingly different income tax structure. The tax rates are presently as follows:

- income between £12,571 and £15, 397 is taxed at 19% (i.e. starter rate)

- income between £15,398 and £27,491 is taxed at 20% (i.e. basic rate)

- income between £27,492 and £43,662 is taxed at 21% (i.e. intermediate rate)

- income between £43,663 and £75000 is taxed at 42% (i.e. high rate)

- income between £75,001 and £125, 140is taxed at 45%(i.e. advanced rate)

- income above £125,140 is taxed at 48% rate (i.e. top rate)

The economic impact of income tax

Income tax is the largest source of tax revenue – contributing nearly a third of the government’s tax receipts. This income is then used to pay for government spending, on things like the police, the NHS and the civil service.

Income tax is a form of aprogressive tax. This means that the proportion of income paid in income tax rises as earnings rise. A simple example below explains a progressive tax. Please do not worry if the calculations below are not clear. You will see more examples later in this session.

Consider two hypothetical workers in England. First worker has a gross income of £25,000 per year, while the second worker earns £100,000 per year. Both gets PA of £12,570. The first worker pays income tax £2,486 (20% on £25000 - £12570 = £12,430). So, overall, this worker’s tax is around 9.9% of the total gross income (i.e. 2486/25000 = 0.099 or 9.9%).

The second worker pays 20% tax on income between £12,570 and £50,270 and 40% tax on the income above £50,270. The total income tax on £100,000 income is then £27,432.2. This is around 27.43% of £100,000 (i.e. 27432/100000 = 0.02743 or 27.43%).

This example shows that the worker earning £100,000 pays a larger percentage of income in tax than the worker earning £25,000. This is the essential idea of a progressive income tax.

In setting income tax rates, the government does need to take into account the impact on the incentive to work. High rates of income tax can deter people from taking on extra work or seeking jobs with greater responsibilities paying higher incomes. People making such decisions will often focus on what extra net income they get – the money in their pocket each month. High tax rates mean they’ll only see small increases and this may mean they’re less likely to do the additional work.

At the end of this session, you will find a link to MoneySavingExpert’s income tax calculator to help you check if you are paying the right amount of tax.