6.3 The household balance sheet

In this section, you will look at how to build the household balance sheet and calculate net worth, the current asset ratio and gearing. You will then find out how to link the balance sheet to the household budget.

Now you’re ready to explore the household balance sheet more fully. This gives an individual or a household a snapshot of their overall financial position at a particular point in time. It also gives clues to how vulnerable the household may be to the financial impact of future shocks. Such information, taken together with cash flow and budgeting statements, is crucial for financial planning.

Take a look at the household balance sheet in your fact find. Let’s take a tour of its components before you start to fill it in with your own details.

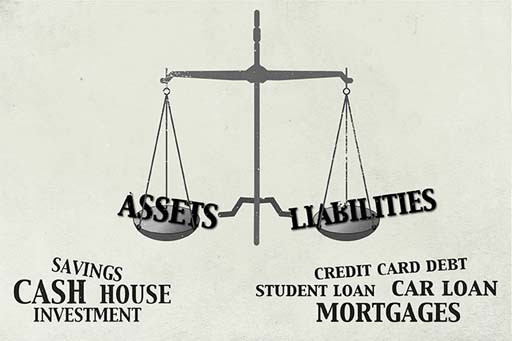

It lists the main items recorded in a financial balance sheet, and most of these items should now be familiar to you. Assets are split between liquid assets and other assets, while liabilities are split between short-term and other liabilities. The difference between total liabilities and total assets provides an estimate of the net worth (or wealth) of an individual or a household – rather like a summary of their overall financial position at a particular point in time.

Note that net worth is estimated rather than a precise calculation, because it can be difficult to obtain an accurate valuation of certain assets without actually selling them. For example, the value of a house can be estimated, but its actual value will depend on a price obtained in the marketplace.

You may also notice that contributions to pension schemes are not included in the assets column. This is because, generally, pensions cannot be sold, cannot be accessed before age 55 and, with some, they are promises of future income rather than pots of savings, making it hard to get a meaningful estimate of their worth. (Pensions are considered separately next in Week 7.)

Despite these reservations, the estimate of net wealth provided by the household balance sheet is useful in giving an overview of an individual’s or a household’s financial position.

Later you’ll look at other calculations related to the household balance sheet – the current asset ratio and gearing – and how these can help with financial planning.