6.3.4 Can gearing predict a crisis?

Let’s start by looking at what happens if house prices fall by 20%. Both households will see the value of their assets fall but there is no change to their liabilities:

- The Sterling family’s home falls in value from £435,000 to £348,000 (which is 80% of £435,000). This is a big drop but the household still has net worth of £436,300 and so still has a large cushion against further shocks. The Sterlings probably do not have to make any immediate changes to their finances.

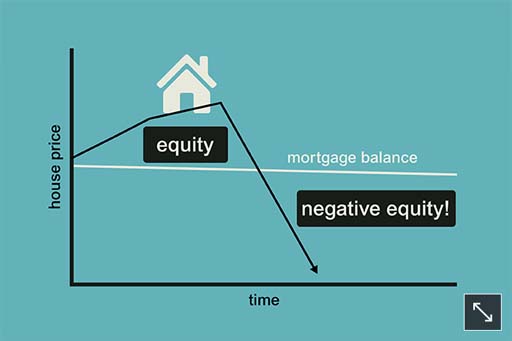

- The Penny family’s home falls in value from £180,000 to £144,000 (which is 80% of £180,000). This leaves them with negative net worth of -£1,150. Moreover, their house is now worth less than their mortgage. The Pennys now have very little scope to cope with further shocks, such as job loss or a major expense, and they cannot afford to move home if they need to.

Could these very different impacts of the same shock on these two households have been predicted? Consider the gearing of each household before the 20% fall in house prices:

The Sterling household has a gearing of £73,900 / £597,200 = 12.4%.

The Penny household has a gearing of £177,200 / £212,050 = 83.6%.

The much higher gearing of the Penny household is a clear indicator that they may be more vulnerable to shocks than the Sterlings. While there is no hard and fast rule about what is a ‘good’ gearing, you should be aware that the higher the ratio, the greater the financial risk to the household.