3.2.3 The relevance of the size of the portfolio

The previous section looked at diversification of a portfolio through investing in three shares. In practice, many more than three shares could be chosen: let’s call the number n. What should n be? The investor should diversify to improve the balance between risk and return, but to what extent?

Suppose that we adopt a simple investment strategy to find out. We invest equal amounts in randomly chosen portfolios that consist of two, three, four, five and more shares. This type of diversification is less efficient than choosing portfolios on the efficient frontier. Indeed, it is an example of naïve diversification: simply choosing to expand the number of shares in the portfolio without examining their risk–return characteristics. The portfolio will not necessarily be Markowitz efficient (see the previous section), but there are still benefits to naïve diversification.

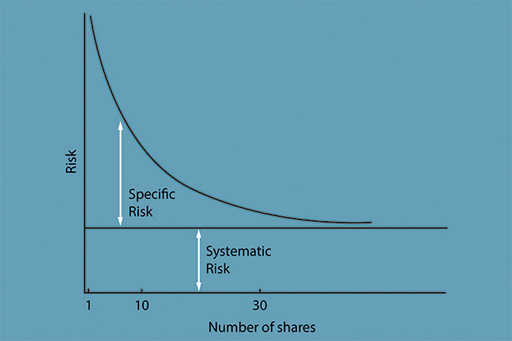

The benefits of naïve diversification can be seen in Figure 4, which plots the typical risk for holding portfolios of one, two, ten, or even up to hundreds of shares, in equal proportions. For example, portfolios consisting of, say, ten shares have less risk than portfolios consisting of one share. Portfolios consisting of thirty shares have less risk than portfolios consisting of ten shares but, beyond that, the benefits to diversification taper off. Why is that? This is because there are common factors affecting all shares that cannot be diversified away: interest rates, economic conditions, tax rates, inflation and so on. Indeed, the benefits of diversification come from diversifying away what is known as specific risk (risk specific to individual companies). A limit is then reached beyond which risk cannot be reduced further. This undiversifiable risk is called systematic risk – risk that is endemic to the stock market and cannot be diversified away, no matter how many shares are included in a portfolio.

The figure has two major implications for investors. First, small investors need only diversify by holding 10 to 15 shares to have substantially reduced the risk from holding just one share. Second, institutional investors do not need to hold vast numbers of shares to be diversified. The extra reduction in risk gained by holding 100 rather than 30 different shares is very small, and may well be more than outweighed by the additional transaction and monitoring costs involved in holding the extra 70 shares.