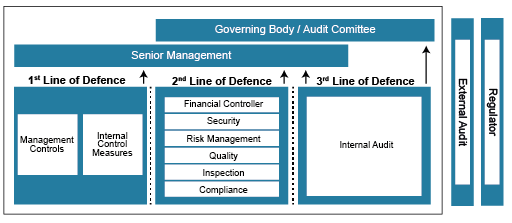

2.2 Risk and assurance – three lines of defence

To ensure the effectiveness of an organisation’s risk management framework, the board and senior management need to be able to rely on adequate line functions – including monitoring and assurance functions within the organisation. The Institute of Internal Auditors (IIA) and the Institute of Directors (IoD) endorse the ‘three lines of defence’ model as a way of explaining the relationship between these functions and as a guide to how responsibilities should be divided. This model is broken down as follows.

- The first line of defence – functions that own and manage risk. Under the first line of defence, operational management has ownership, responsibility and accountability for directly assessing, controlling and mitigating risks.

- The second line of defence – functions that oversee or specialise in risk management and compliance. The second line of defence consists of activities covered by several components of internal governance (compliance, risk management, quality, IT and other control departments). This line of defence monitors and facilitates the implementation of effective risk management practices by operational management and assists the risk owners in reporting adequate risk-related information up and down the organisation.

- The third line of defence – functions that provide independent assurance. An independent internal audit function will, through a risk-based approach to its work, provide assurance to the organisation’s board of directors and senior management. This assurance will cover how effectively the organisation assesses and manages its risks and will include assurance on the effectiveness of the first and second lines of defence. It encompasses the entire framework, the operation of the framework and the coverage and all categories of organisational objectives.