2.5 T-accounts, debits and credits

What do all accounts look like in a double-entry system?

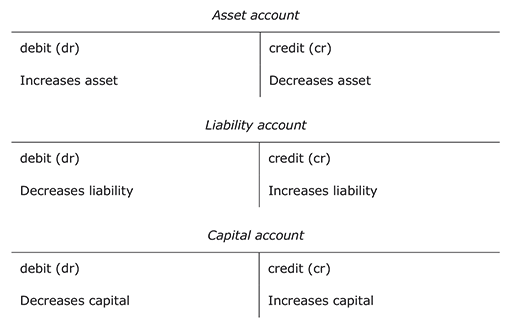

Traditional double-entry bookkeeping divides every account into two halves as follows:

This T appearance has led to the convention of ledger accounts being referred to as T-accounts.

Convention, which has not changed for hundreds of years, prescribes that the left-hand side of a T-account is called the debit side, and the right-hand side is called the credit side.

What is the main reason that all accounts are divided into a left or debit side and a right or credit side?

As we have seen in Sections 2.3 and 2.4, because of the dual aspect of double-entry bookkeeping, if one account changes as a result of a financial transaction, then another account needs to change to keep the accounting equation in balance. This is shown in ledger or T-accounts by recording each transaction twice, once as a debit-entry in one account and once as a credit-entry in another account. This is done according to time-honoured rules which treat asset accounts differently from liability accounts and the capital account.

What are the rules of double-entry bookkeeping?

If a transaction increases an asset account, then the value of this increase must be recorded on the debit or left side of the asset account. If, however, a transaction decreases an asset account, then the value of this decrease must be recorded on the credit or right side of the asset account. The converse of these rules applies to liability accounts and the capital account, as shown in the three T-accounts below:

Pause for thought

These rules need to be memorised initially as they are not intuitive. Through seeing how they work in practice and doing exercises they will become second nature – a little bit like learning to swim or ride a bicycle.

The balance on an asset account is always a debit balance. The balance on a liability or capital account is always a credit balance. (Later on in this section you will learn how to work out the final or closing balance on an account which has both debit and credit entries. The process of determining the closing balance on an account is known as ‘balancing off ’ an account.)

The best way to understand how the rules of double-entry bookkeeping work is to consider an example. We will now record the six transactions carried out by Edgar Edwards Enterprises in the appropriate T-accounts.

Example

Transactions:

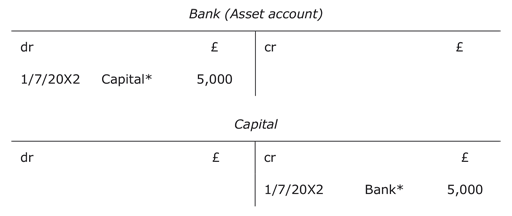

- The owner starts the business with £5,000 paid into a business bank account on 1 July 20X2.

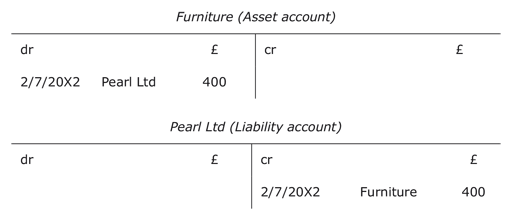

- The business buys furniture for £400 on credit from Pearl Ltd on 2 July 20X2.

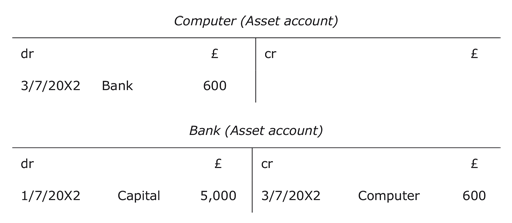

- The business buys a computer with a cheque for £600 on 3 July 20X2.

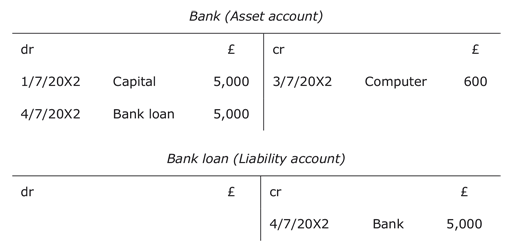

- The business borrows £5,000 on loan from a bank on 4 July 20X2. The money is paid into the business bank account.

- The business pays Pearl Ltd £200 by cheque on 5 July 20X2

- The owner takes £50 from the bank for personal spending on 6 July 20X2.

Transaction 1 : The owner starts the business with £5,000 paid into a business bank account on 1 July 20X2. (Following the rules we learnt, we thus need to debit an asset account and credit the capital account.)

* Each T-account, when recording a transaction, names the corresponding T-account to show that the transaction reflects a double entry in the nominal ledger.

Transaction 2 : The business buys furniture for £400 on credit from Pearl Ltd on 2 July 20X2. (We need to debit an asset account and credit a liability account.)

Transaction 3 : The business buys a computer with a cheque for £600 on 3 July 20X2. (We need to debit an asset account and credit an asset account.)

Transaction 4 : The business borrows £5,000 on loan from a bank on 4 July 20X2. The money is paid into the business bank account. (We need to debit an asset account and credit a liability account.)

Transaction 5 : The business pays Pearl Ltd £200 by cheque on 5 July 20X2. (We need to debit a liability account and credit an asset account.)

Transaction 6 : The owner takes £50 from the bank for personal spending on 6 July 20X2. (We need to debit the capital account and credit an asset account.)

In Section 2.3 we recorded the consequences of these transactions in a balance sheet for Edgar Edwards Enterprises dated 6/7/20X2. Did you find it easy to do that? As there were only six transactions, it was probably not too difficult. However, many enterprises have to record hundreds of transactions per day. Having individual T-accounts within the nominal ledger makes it much easier to collect the information from many different types of transactions. The next section will explain what is done with the balances in each of these accounts.