14 Failure to prevent tax evasion

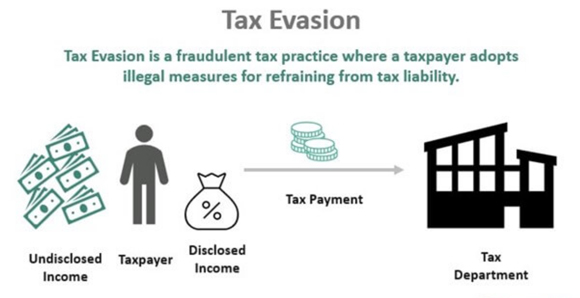

As Figure 10 shows, ‘tax evasion’ refers to using illegal ways to pay less tax than you should. ‘Tax avoidance’ refers to using legal ways to reduce your tax liability.

Under the Criminal Finances Act 2017, failure to prevent the facilitation of tax evasion is a criminal offence. This means that this offence can make a ‘relevant body’ criminally liable if it fails to prevent UK or non-UK tax evasion by an employee or ‘associated person’ (Kaplan, 2022, p. 258).

Box 7 Section 44, Criminal Finances Act 2017

44 Meaning of relevant body and acting in the capacity of an associated person

- This section defines expressions used in this Part of the Act.

- ‘Relevant body’ means a body corporate or partnership (wherever incorporated or formed).

- ‘Partnership’ means—

- a.a partnership within the meaning of the Partnership Act 1890, or

- b.a limited partnership registered under the Limited Partnerships Act 1907, or a firm or entity of a similar character formed under the law of a foreign country.

- A person (P) acts in the capacity of a person associated with a relevant body (B) if P is—

- a.an employee of B who is acting in the capacity of an employee,

- b.an agent of B (other than an employee) who is acting in the capacity of an agent, or

- c.any other person who performs services for or on behalf of B who is acting in the capacity of a person performing such services.