6 Internal controls to prevent money laundering

Internal controls are policies and procedures an organisation has in place to ensure that its systems operate as efficiently and effectively as intended, its assets are safeguarded, and it is complying with all applicable laws and regulations (Arens, Elder and Beasley, 2014).

Designing and implementing robust controls is essential for ensuring accountability. The UK Corporate Governance Code requires directors of listed organisations to design and implement a sound internal control and risk management system (FRC, 2024).

The Association of Certified Fraud Examiners (2022) highlighted that almost half of the fraud cases covered by its global fraud study could be attributed to either a lack of internal controls (29%) or the overriding of existing controls (20%). If firms adopt effective internal controls, money laundering can also be avoided.

There are various types of controls that could combat money laundering effectively. One of the most important components is monitoring.

Besides monitoring, there are some other additional anti-money laundering controls that can be used, including:

- external audit of financial statements

- internal audit department

- external audit of internal controls over financial reporting

- an independent audit committee

- an anti-money laundering policy

- anti-money laundering training

- an employee support programme

- a dedicated anti-money laundering department, function or team

- management review

- customer due diligence where accountants ask clients to provide satisfactory evidence to verify their identity

- rewards for whistle-blowers.

Furthermore, firms are legally obliged to appoint a money laundering compliance principal (MLCP) and a money laundering reporting officer (MLRO). These officers can help firms assess the likelihood of money laundering and report any suspicious activities to relevant authorities. However, the requirement to appoint a MLCP and a MLRO is subject to the ‘size and nature’ of the business.

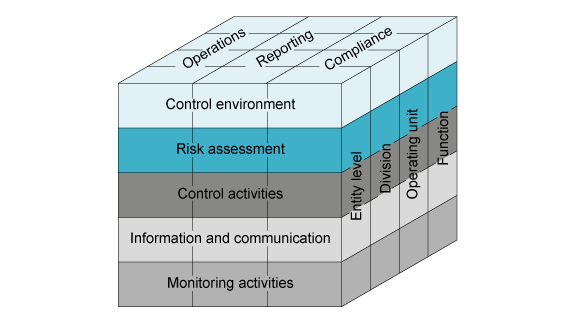

A framework for internal controls was developed, and subsequently revised, by the Committee of Sponsoring Organisations of the Treadway Commission (COSO, 2013a).

The COSO Internal Control Integrated Framework (see Figure 6) recognised five components of internal control:

- the control environment

- risk assessment

- control activities

- information and communication

- monitoring activities.

Generally speaking, all five components must be present, functioning and operating together to conclude that internal control is effective (Arens, Elder and Beasley, 2014).

You will examine each of these components in turn.