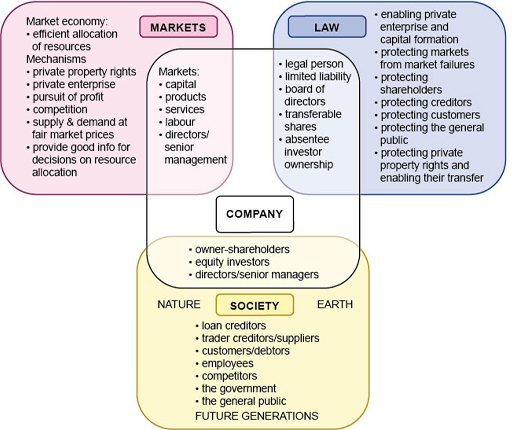

2 The market environment and sources of company finance

The economic environment in which companies operate in market economies is characterised by markets for goods, services, labour, senior managers and, last but not least, capital. In market economies, the assumption is that private property rights, competition, the pursuit of profit, and market prices that are set through the forces of supply and demand are the best way to bring about an efficient allocation of resources in the economy.

Different markets will have different characteristics which are outside the scope of this course. However, it is important to note that market prices of goods and raw materials, both historic and current, are important in determining the financial position and financial performance of a company. Similarly, the market prices of services and labour play a vital role in determining company success. In addition, the market for senior managers is relevant for large and listed companies where there is a clear separation between the ownership of the company’s shares and the control of its resources.

Finally, companies raise their debt and equity capital in capital markets. Financial reporting is one of the main sources of information for investors on which to base their decisions. Because companies are not likely to provide financial reports that are comparable and because managers and shareholders do not have the same information about the company, financial reporting standards and capital market regulations are necessary to protect the interests of investors, lenders, creditors and other company stakeholders.

Figure 5 summarises the discussion on the market, legal and social context of company financial accounting so far.