8 The nature of production costs: materials, labour and overheads

Production costs can be classified into three broad categories: materials, labour and overheads. These costs will be captured on a cost card. The cost card is a summary of costs that together make the total cost of one unit of a product – for example, a television or a meal. The term cost card is from an age that pre-dates computers, when costs were summarised on cards as they were incurred in the production process. Today, cost cards are embedded within accounting software with various coding systems, but the principle remains the same and the same information is recorded.

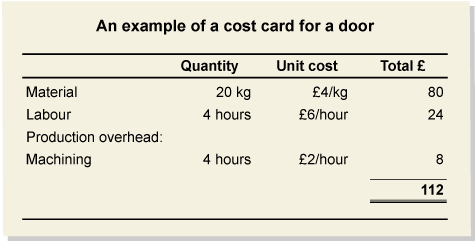

The information recorded constitutes the basic elements of cost: the materials used, the cost of labour and the proportion of indirect costs attributable to a particular unit of output. The source of this information is described in the next few sections. See the example below of a cost card for a door (figures are assumed).

You certainly need to understand the basic way in which cost data is captured. The broad categories of cost in an organisation are covered in the next three sections.