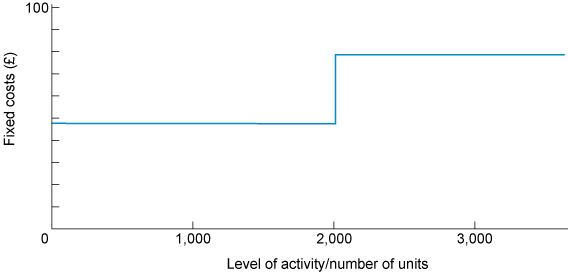

2.2 Stepped fixed costs

Fixed costs are often only fixed within a range of activity levels, i.e. the relevant range. Fixed costs are often assumed to be fixed whatever the level of activity, but they do change. The term used to describe the concept of change in fixed costs is ‘stepped costs’. These can be described as being constant within a specified range of output but changing when outside this range, as illustrated in Figure 8, where above 2,000 units a new level of fixed costs is reached.

The concept of stepped costs can be illustrated by an accounting practice. For a given level of clients, the practice can cope with the current number of accountants, but at a certain level of activity, the pressures of work will mean an additional accountant needs to be employed. If on a full-time contract, this extra accountant would be a stepped cost – that is, an increased fixed cost. (If an accountant could be employed on a casual, part-time basis, this would resemble more closely a variable cost.)