9.4 EMA process

Tracking environmental costs facilitates the understanding of links between costs and provides insights into cost reductions through specific actions on cost drivers. In most management accounting systems, however, environmental costs are hidden within general overheads; thus relationships are not identified. It is vital to allocate environmental costs to the processes or products which give rise to them. Only by doing this can an organisation make well-informed business decisions and improve controls and benchmarking. Techniques such as input/output analysis can help organisations balance resources and costs, making them more transparent and manageable.

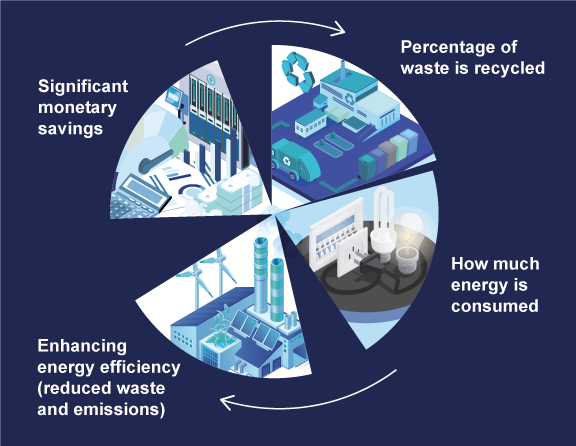

For example, a manufacturing company should know exactly how much waste is created during a production process, what percentage of the waste is recycled and how much energy is consumed. Only by identifying and allocating such costs to individual production processes can the company make informed decisions about the environmental effects of its activities. Enhancing efficiency in the use of energy, water and other raw materials brings not only environmental improvements (reduced resource use and reduced waste and emissions), but also potentially significant monetary savings as the costs of purchase and waste treatment decrease.

Bennett and James (1998) suggested that the process of EMA involves three key levels: the gathering of environmental data (lowest level), the conversion of this data into useful information (middle level) and the dissemination of this information to decision makers, i.e. managers (top level).